Working capital can quietly change the seller’s proceeds.

The adjustment can move both ways.

What is included and excluded matters.

The estimate at closing may not be the final answer.

The buyer should not get unchecked control over the final calculation.

You just signed the letter of intent, and the price listed there is $5 million. You can already picture that much-needed vacation after building your business to this point.

But depending on the terms of yourasset purchase agreement, that number may assume you will deliver the business with a certain level of working capital and with specificassets andliabilitiesincluded or excluded.

In other words, the number in the letter of intent is not always the amount you will actually walk away with. The purchase price adjustment in your asset purchase agreement can increase or decrease your sale proceeds. Here is how that works.

What Is a Purchase Price Adjustment?

A purchase price adjustment is a mechanism in an asset purchase agreement that changes the final purchase price if the business is delivered with a different level of working capital, or with different assets or liabilities, than the parties expected.

In simple terms, it is a way to compare the financial condition the buyer thought it was getting with what the buyer actually receives at closing. If the business is delivered with less working capital than expected, the purchase price may go down. If it is delivered with more, the purchase price may go up.

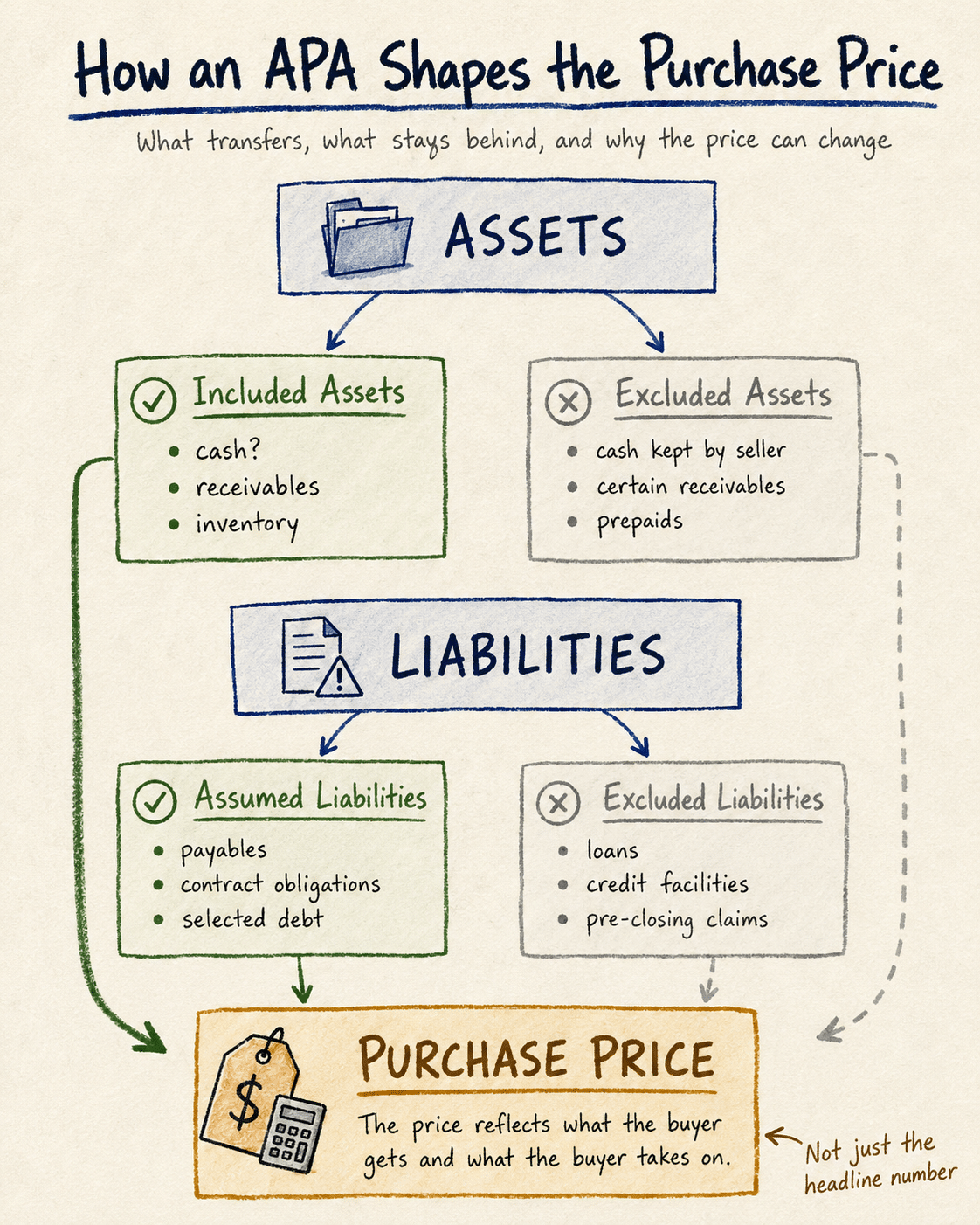

The Asset Purchase Agreement Defines What the Buyer Gets and Takes On

To understand why the adjustment can change the final price, you first need to understand what the buyer is actually receiving in the asset purchase agreement.

An asset purchase agreement defines what the buyer receives, what the seller keeps, which liabilities the buyer assumes, and which liabilities stay behind.

Unlike a stock purchase agreement, where the buyer acquires the company with its underlying assets and liabilities, an asset purchase agreement lets the parties define what will transfer and what will stay behind.

That distinction matters because the purchase price is tied to the specific assets, liabilities, and net assets included in the transaction. Before you understand how the purchase price adjustment works, you need to understand what the buyer is actually getting and what obligations the buyer is taking on.

Included Assets Affect What the Buyer Is Paying For

Your asset purchase agreement should define the purchased assets that will transfer to the buyer at closing. Depending on the target business, those assets may affect the purchase price, the working capital calculation, and the final economics of the sale.

Purchase assets may include:

Accounts receivable: If you and the buyer agree on a $1 million purchase price, but customers still owe the business $150,000 for work performed before closing, the agreement should say who gets the right to collect that money and whether receivables are counted in working capital.

Inventory: If the buyer expects to receive inventory, the asset purchase agreement should say how that inventory is included, how it is valued, and whether obsolete or slow-moving inventory is treated differently. Inventory may also affect the working capital adjustment if it is treated as a current asset in the net working capital calculation.

Equipment: Also known as tangible personal property, may include office furniture, vehicles, tools, machinery, computers, and other property needed to operate the business. The asset purchase agreement should make clear what equipment is included, whether it is owned or leased, and whether it is in usable condition.

Contracts: Contracts matter because they may carry future revenue, customer relationships, supplier access, or operating rights. But contracts do not always transfer automatically. The agreement should identify which contracts are assigned to the buyer and whether any third-party consent is needed. If an important contract cannot be assigned, that may affect the value of the deal.

Books and records: They may not look valuable in the same way as cash or inventory, but can be essential after closing. Customer records, accounting records, pricing history, supplier lists, operating files, and correspondence may help the buyer run the business, collect receivables, verify obligations, and respond to later disputes.

Goodwill: Goodwill is the intangible value of the business. It is tied to customer relationships, reputation, brand recognition, and the fact that the business is already operating. If goodwill is included, the buyer is also buying the business’s existing market position.

Excluded Assets Affect What the Seller Keeps

If the seller wants to keep certain assets, those assets need to be identified in the asset purchase agreement.

Examples may include:

Cash: If you agree on a $1 million purchase price and the buyer also receives $100,000 in cash at closing, the seller may argue that the buyer is really receiving $1.1 million in total value. Many asset purchase agreements address this issue by excluding cash from the purchased assets.

Certain receivables: A seller may want to keep receivables connected towork performed before closing. That makes sense from the seller’s view because the seller earned that revenue before the sale.

Prepaid items: These are expenses that the seller already paid before closing, but that the buyer may benefit from after closing, such as rent, subscriptions, or vendor deposits.

Assumed Liabilities Affect the Buyer’s Real Cost

Just as important, your asset purchase agreement should define the liabilities the buyer assumes at closing. If the buyer pays $5 million at closing and also assumes $1 million in liabilities, the buyer may view the transaction as a $6 million commitment. That is why assumed liabilities have to be read together with the purchase price.

Examples of assumed liabilities may include:

Accounts payable: These are unpaid bills owed by the business. For example, the seller may owe vendors $75,000 for goods delivered before closing. If the buyer assumes those payables, the buyer is taking on a payment obligation in addition to the purchase price.

Contract obligations: If the buyer takes over a customer contract, the buyer may have to deliver products, provide services, honor warranties, or satisfy prepaid obligations. Those obligations can affect the real cost of the deal.

Selected debt: In many asset purchase agreements, seller debt is excluded unless the buyer expressly agrees to assume it. But sometimes the buyer may agree to take on selected debt, such as equipment financing, a vehicle loan, or another obligation tied to an asset the buyer wants.

Excluded Liabilities Affect What Stays Behind

Excluded liabilities help protect the buyer from paying for obligations that were not part of the deal. They should be clearly identified in the asset purchase agreement so the parties know which liabilities remain with the seller after closing.

Examples may include:

Seller debt: Seller debt should be addressed clearly. If the seller borrowed money before closing, the agreement should say whether that debt stays with the seller or whether the buyer has agreed to assume it.

Loans: Loans can include bank loans, equipment loans, vehicle loans, or other borrowed amounts connected to the business. The main issue is whether the buyer is taking the asset without the loan, or taking both the asset and the repayment obligation.

Credit facilities: A credit facility is a line of credit or other borrowing arrangement the business uses for working capital or operations. If that borrowing stays with the seller, it should not become part of the buyer’s post-closing cost.

Pre-closing claims: These are claims tied to events that happened before the closing date, such as customer disputes, vendor claims, employee claims, or tax issues. If those claims stay with the seller, the buyer should not have to absorb them after closing unless the purchase agreement says otherwise.

Transaction costs: These are costs tied to the sale process, such as legal fees, accounting fees, advisor fees, or broker fees. The asset purchase agreement should say whether those costs stay with the seller, are paid at closing, or are handled separately from the working capital adjustment.

How Included Assets and Assumed Liabilities Affect Working Capital

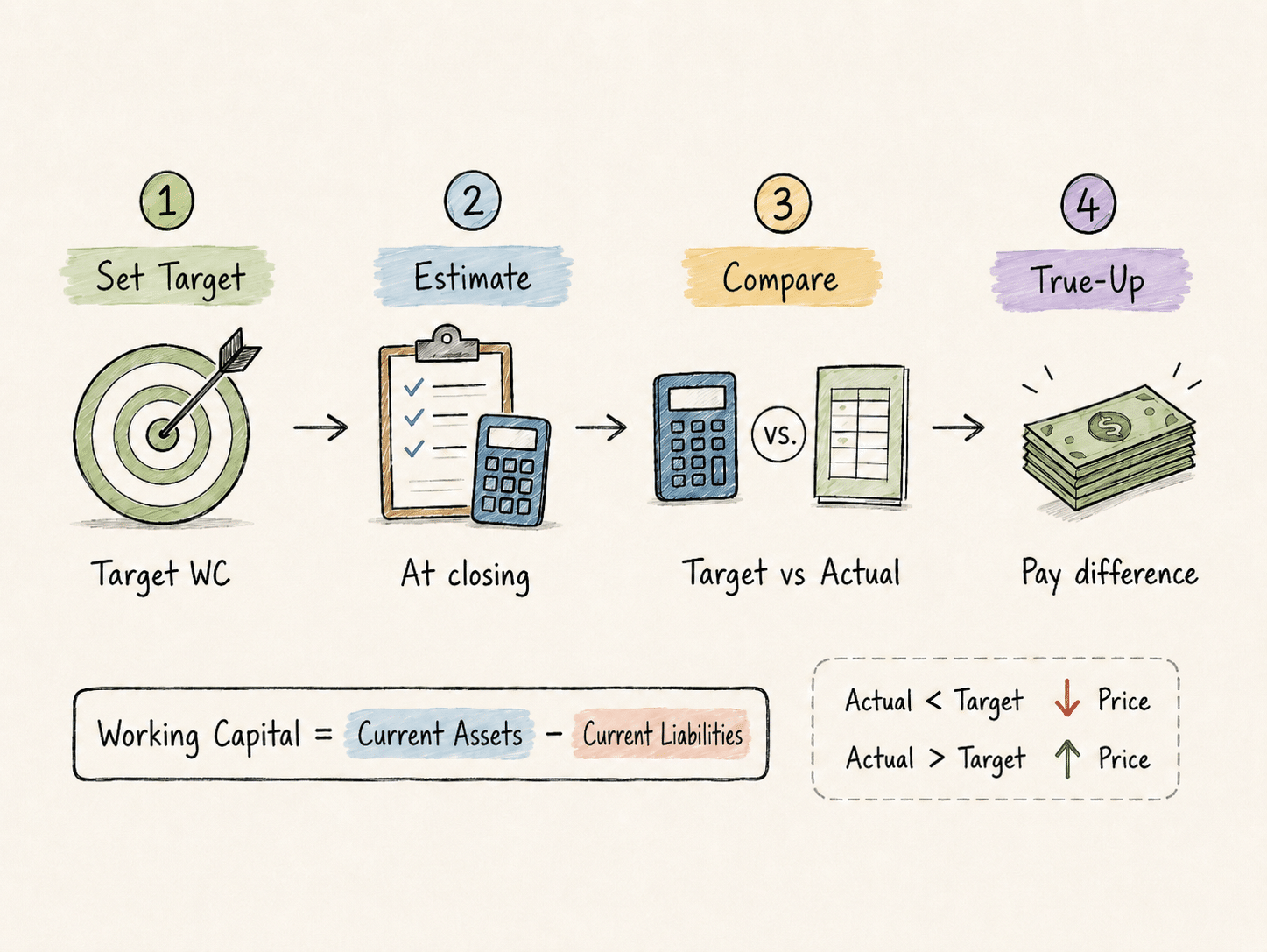

Working capital usually refers to the short-term assets and short-term liabilities the business uses in ordinary operations. The basic formula is:

Working capital = current assets minus current liabilities

In many asset deals, the purchase agreement sets a target net working capital amount that must be delivered to the buyer at closing. That target working capital is usually based on the current assets included in the sale and the current liabilities the buyer assumes. Because working capital can change between signing and closing, the seller’s obligation to operate the business in the ordinary course before closing may affect the assets and liabilities ultimately delivered to the buyer.

How the Price Adjustment Mechanism Works in an Asset Purchase Agreement

The purchase price adjustment mechanism tests whether the target business is being delivered in the financial condition the parties priced.

One financial measure used to test that condition is working capital, which we defined above. Working capital is different from the purchase price. The purchase price is the headline number for the transaction. Working capital is the short-term financial measure used to see whether the buyer is receiving the business with the current assets and current liabilities the parties expected at closing.

Example: How the Purchase Price Adjustment May Decrease the Final Price

Assume the asset purchase agreement says:

Item

Amount

Base purchase price

$5,000,000

Target working capital

$500,000

That means the $5 million base purchase price assumes the buyer will receive the target business with $500,000 of working capital at closing.

At closing, the buyer receives these included current assets:

Current assets included

Amount

Accounts receivable

$250,000

Inventory

$300,000

Prepaid expenses

$50,000

Total current assets

$600,000

The buyer also assumes these current liabilities:

Current liabilities assumed

Amount

Accounts payable

$100,000

Accrued expenses

$50,000

Total current liabilities

$150,000

So actual working capital is:

$600,000 minus $150,000 = $450,000

The target working capital was $500,000.

That means the buyer received $50,000 less working capital than the purchase price assumed.

So the purchase price may be adjusted downward by $50,000:

Item

Amount

Base purchase price

$5,000,000

Less working capital shortfall

($50,000)

Adjusted purchase price

$4,950,000

Example: How the Purchase Price Adjustment May Increase the Final Price

If the target working capital is still $500,000, but the business is delivered with $575,000 in actual working capital at closing, the buyer receives $75,000 more working capital than the purchase price assumed.

In that case, the seller may seek an upward purchase price adjustment:

Item

Amount

Base purchase price

$5,000,000

Plus working capital excess

$75,000

Adjusted purchase price

$5,075,000

So the purchase price adjustment does not automatically favor the buyer or the seller. It depends on the difference between the target working capital and the actual working capital delivered at closing.

How the Purchase Price Adjustment Process Works

A working capital adjustment compares the target amount to the actual amount at closing, then adjusts the purchase price up or down based on the difference.

The purchase price adjustment does not usually happen all at once. It is a process that starts before closing and may continue after the buyer takes over the business.

Step 1: The Asset Purchase Agreement Sets the Target

The asset purchase agreement first sets the target working capital. This is the amount of working capital the buyer is expected to receive with the business at closing.

Step 2: Before Closing, the Seller Estimates the Closing Numbers

Before closing, the seller usually prepares an estimated closing statement. That statement estimates what the working capital will be on the closing date.

The parties use that estimate to determine how much should be paid at closing.

Step 3: At Closing, the Purchase Price Is Adjusted Based on the Estimate

At closing, the parties compare the estimated working capital against the target working capital.

If the estimate is lower than the target, the buyer may pay less at closing.

If the estimate is higher than the target, the buyer may pay more at closing.

Step 4: After Closing, the Buyer Prepares the Final Calculation

After closing, the buyer has control of the business and access to the books. The buyer then prepares the final working capital calculation.

This is necessary because the closing payment was based on an estimate. After closing, the parties check the actual numbers.

The question becomes:

Did the buyer actually receive the working capital the seller estimated?

Step 5: The Final Number Is Compared to the Estimate

The post-closing true-up compares the final closing working capital to the estimated closing working capital.

If the final number is lower than the estimate, the seller may owe money back to the buyer.

If the final number is higher than the estimate, the buyer may owe more money to the seller.

Step 6: The Seller Gets a Chance to Review the Buyer’s Calculation

The buyer does not usually get the final word automatically. The seller should have a review period to examine the buyer’s calculation.

The seller may review the closing statement, books and records, and supporting financial information. If the seller disagrees, the seller can object.

Common disputes may involve whether certain receivables should count, whether inventory was valued correctly, whether debt was treated properly, or whether certain accrued expenses belong in current liabilities.

Step 7: Unresolved Disputes May Go to an Independent Accountant

If the buyer and seller cannot resolve the dispute, the agreement may send the disputed items to an independent accountant.

This process is usually meant for accounting disputes, not every possible legal issue. For example, the independent accountant may decide whether a disputed receivable should be included or whether a liability was properly counted.

Step 8: The Final Adjustment Is Paid

Once the final amount is determined, money moves in the right direction.

If the adjustment favors the buyer, the seller may have to pay the buyer.

If the adjustment favors the seller, the buyer may have to pay the seller.

That final payment is the true-up. It corrects the difference between the estimated numbers used at closing and the actual numbers finally determined after closing.

Speak to Our New Jersey Business Lawyers Today

A purchase price adjustment can pull you back into the asset sale after closing. The closing payment may not be the final amount you receive.

If the buyer reviews the books after closing and the financial data shows that the business delivered less working capital than the purchase price assumed, you may face a negative adjustment. In some cases, that may mean paying money back to the buyer.

That is why the purchase price adjustment mechanism should be reviewed before the asset purchase agreement is signed.

Are you wondering about any of the issues mentioned above? Please email us at info@wilkinsonlawllc.com or call (732) 410-7595 for assistance.

AtWilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthybusiness advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQ

Who Benefits From a Purchase Price Adjustment, the Buyer or the Seller?

It can benefit either side. A buyer may benefit if the business is delivered with less working capital than promised. A seller may benefit if the business is delivered with more working capital than the agreed target. The adjustment is not supposed to be a penalty. It is meant to compare the target working capital against the actual working capital delivered at closing.

Should Cash Be Included in Working Capital?

Not always. Many asset purchase agreements exclude cash because the deal is intended to be cash-free. But the agreement needs to say that clearly. If cash is included, it may increase the working capital delivered to the buyer or otherwise affect the purchase price. If cash is excluded, the seller usually keeps it.

What Happens if the Buyer and Seller Disagree Over the Final Calculation?

The asset purchase agreement should provide a process. Usually, the seller gets a review period after the buyer prepares the final calculation. If the seller disagrees, the seller can object within the deadline. If the parties still cannot resolve the disputed items, the agreement may send the dispute to an independent accountant.

What Should a Seller Review Before Agreeing to a Purchase Price Adjustment?

A seller should pay close attention to the mechanics of the adjustment, including:

the target working capital;

which assets are included in the calculation;

which liabilities are included in the calculation;

who prepares the estimated closing statement;

who prepares the final true-up;

the deadline for objecting; and

whether disputed items go to an independent accountant.

The seller should also check whether cash, debt, receivables, prepaid items, accrued expenses, and deferred revenue are being treated consistently.

Is the Target Net Working Capital Number Negotiable?

Yes. Target working capital is often negotiated because it affects the final economics of the deal. A higher target can make it easier for the buyer to claim a shortfall. A lower target may reduce the chance of a downward adjustment. The number should be based on the business’s actual financial data, ordinary course operations, and any seasonal fluctuations that affect working capital.

When Is the Purchase Price Finally Determined?

The purchase price may not be final until the post-closing true-up process is complete. That may happen after the buyer prepares the final calculation, the seller’s review period ends, any objections are resolved, and any required payment is made. If there is a dispute, final determination may take longer.