Signing an asset purchase agreement does not always end your control of the business, but it can limit what you do before closing.

The ordinary course of business provision requires the seller to keep operating the business in a manner consistent with how it was run before signing.

In an asset sale, the agreement should clearly define the business being protected.

The APA may restrict specific seller actions before closing, including selling purchased assets, taking on unusual debt, or giving up contract rights.

Buyer consent may give the seller a way to move forward with a restricted decision.

Disclosure schedules matter when the seller already knows something will change before closing.

After signing an asset purchase agreement, the seller may still need to operate the business in the ordinary course until closing.

You signed an asset purchase agreement, but closing is still two months away.

The business has not stopped moving just because the agreement is in place. Employees still need direction and customers still call. And if the sale is almost done, cutting back on advertising may seem reasonable. Holding off on a repair may feel practical when you do not expect to own the equipment much longer.

The buyer may see it differently.

It agreed to buy the business based on what it reviewed during due diligence, including thepurchased assets,customer relationships,financial condition, and day-to-day operations. If those things change before the closing date, the buyer may argue that the seller’s business no longer looks like the business it agreed to buy.

That is why the ordinary course of business language in yourasset purchase agreement matters. During the period between signing and closing, your purchase agreement may require seller actions to remain consistent with past practice or obtain buyer consent before making certain decisions.

This article explains how an ordinary course of business asset purchase agreement provision can limit what you do before closing, why the buyer cares about preserving the purchased assets, and how unclear language about “the Business” can lead to future disputes.

What “Ordinary Course of Business” Means in an Asset Sale

In an asset purchase agreement, “ordinary course of business” means the seller keeps operating the business in the same basic manner it operated before the agreement was signed.

But the harder question is: ordinary for which business?

In a stock sale, the buyer is usually acquiring ownership of the entire legal entity. That can make the definition of the business easier to understand because the company itself is what changes hands.

In an asset sale, the buyer may purchasespecific assets and assume onlyselected liabilities. The purchase agreement may cover two locations, one product line, contracts, equipment, customer lists, intellectual property, or another defined part of the seller’s business.

That distinction matters.

If your business has ten locations and you are selling two, a decision that makes sense for the company as a whole may still affect the locations being sold.

That is why your asset purchase agreement should define which business the ordinary course applies to. If the language is vague,the disagreement may begin with the definition before anyone even gets to whether your decision was reasonable.

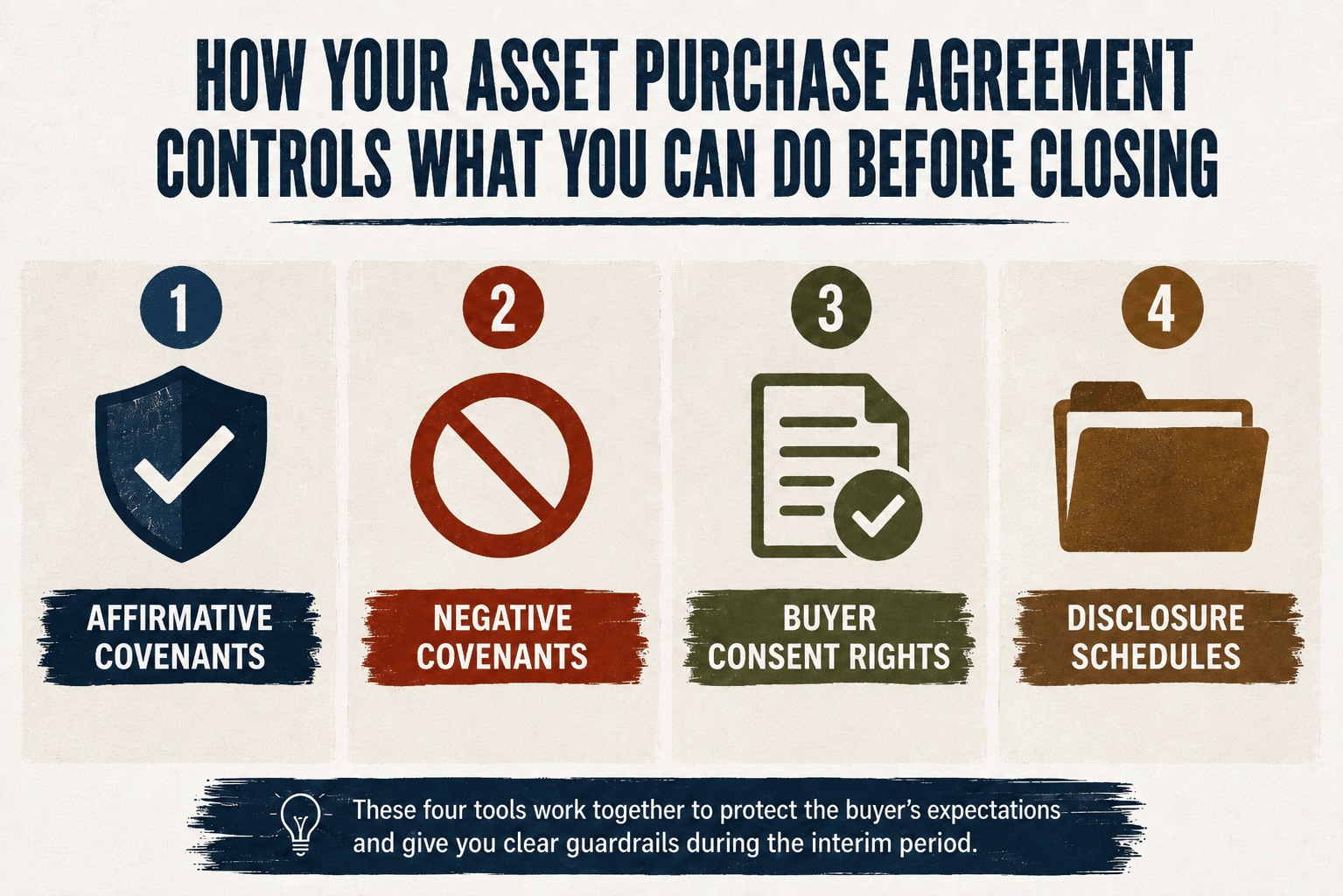

How the Asset Purchase Agreement Restricts Seller Decisions Before Closing

An asset purchase agreement may use covenants, consent rights, and disclosure schedules to guide what the seller can do before closing.

Your asset purchase agreement may separate the signing date from the closing date and say what you can and cannot do while the buyer is waiting to receive the business.

Here is how:

Affirmative Covenants: Keep the Business Going Properly

The first tool your asset purchase agreement uses is an affirmative covenant. This tells you what you must keep doing from the signing date to closing.

In this context, the agreement may require you to:

Conduct the Business in the ordinary course

Maintain and preserve the Business

Preserve rights,goodwill, and business relationships

These obligations are there because the buyer agreed to the asset purchase based on what it saw before signing.

Negative Covenants: Do Not Make Certain Changes Before Closing

Your asset purchase agreement may also stop you from taking specific actions between signing and closing. These are negative covenants. They do not simply say, “keep running the business.” They identify changes the seller cannot make unless the agreement allows them, the disclosure schedules carve them out, or the buyer gives consent.

Depending on the language in your APA, the restricted actions may include:

Taking actions that could create a material adverse effect This means you should not make a decision that materially harms the business, the purchased assets, the financial condition of the business, or your ability to complete the deal. Changes to accounts receivable, inventory, accounts payable, or other working capital items may also affect the amount the seller ultimately receives through a purchase price adjustment.

Taking on unusual debt Many asset purchase agreements restrict the seller from incurring debt connected to the Business above a stated dollar amount before closing.

Selling or disposing of purchased assets The agreement may prohibit you from selling assets shown on the balance sheet or included in the purchased assets, except for ordinaryinventory sales or other exceptions stated in the APA.

Giving up debts, claims, or rights tied to the purchased assets This can include contract rights, payment claims, warranties, customer rights, or other valuable rights the buyer expects to receive.

Making large capital expenditures that becomeassumed liabilities The issue is not only the spending itself. The issue is whether the buyer will be expected to take on the financial obligation after closing.

Buyer Consent: You May Need Written Approval Before Making the Change

If a restricted decision needs to be made before closing, that does not always mean you are stuck. The asset purchase agreement may let you move forward if the buyer gives written consent.

Suppose a piece of expensive equipment included in the purchased assets breaks down before the closing date. You may not want to spend money repairing equipment you are about to transfer to the buyer. Selling that equipment and leasing a replacement for the interim period may feel like the practical business decision.

In that situation, your APA may require you to get written consent from the buyer before you act.

Disclosure Schedules: Disclose Known Exceptions Before They Become Problems

You may already know before signing that something will change before closing.

A key employee may be leaving next month.

A customer contract may be under renegotiation.

A piece of equipment may need to be replaced, or inventory may drop because of a large pending order.

If you sign the APA without addressing those known changes, the buyer may later say, “You were supposed to operate in the ordinary course. You did not tell us this was going to happen.”

That is where disclosure schedules matter. A disclosure schedule is attached to the asset purchase agreement. It contains exceptions, details, qualifications, and deal-specific disclosures that show how the written promises apply to the actual transaction.

Speak With Our New Jersey and New York Business Attorneys Today

If you signed an asset purchase agreement, or you are about to sign one, the period between signing and closing deserves careful attention. The agreement may restrict certain seller actions until the closing date, and the exact limits depend on the language of your deal.

That means you need to know which decisions remain part of normal business operations and which ones require more care. Buyer consent rights may give you a way to move forward when a restricted decision needs to be made. Disclosure schedules may also let you identify known exceptions before they become disputes.

Are you wondering about any of the issues mentioned above? Please email us at info@wilkinsonlawllc.com or call (732) 410-7595 for assistance.

AtWilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthybusiness advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQ

What Should I Do if I Need to Make an Urgent Business Decision Before Closing?

Check the APA before acting. If the decision affects purchased assets, contracts, employees, assumed liabilities, or post-closing operations, document the reason and request written consent.

Can the Buyer Refuse Consent Just to Gain Leverage Before Closing?

Many APAs say buyer consent cannot be unreasonably withheld, conditioned, or delayed. The buyer should have a deal-related reason for refusing consent or adding conditions.

What Happens if I Violate an Ordinary-Course Covenant Before Closing?

The buyer may delay closing, refuse to close if a condition fails, demand a cure, renegotiate terms, or raise an indemnification claim after closing.

Should I Tell the Buyer About a Planned Change Even if I Think It Is Minor?

Yes, if the change affects the business being sold. A small change can matter if it touches a key contract, employee, customer relationship, or purchased asset.