Treat an earn-out as conditional purchase price, not guaranteed money. Read the closing payment and any potential earn-out payments separately.

Do not rely on the maximum earn-out amount alone. Caps, minimum payments, all-or-nothing formulas, and missed-period rules can change what is actually payable.

Make sure the earn-out metric matches what the buyer is actually acquiring. Revenue, EBITDA, net income, customer retention, and milestones can each shift risk differently.

Pay close attention to buyer control after closing. Post-closing covenants, separate records, customer treatment, and key employee provisions can affect whether the earn-out target is reached.

Check how the earn-out will be calculated, challenged, and paid. Reporting rights, objection deadlines, accounting procedures, offsets, escrow, and acceleration language can determine whether you actually receive an earned amount.

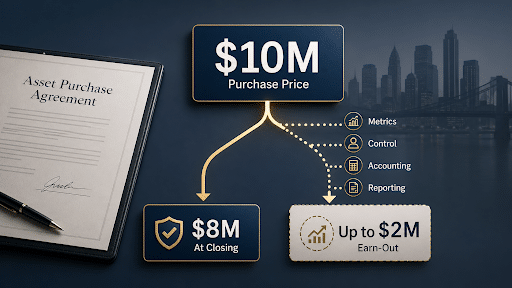

You may be selling your business and view the earn-out provision in your asset purchase agreement as the final part of the purchase price. Or you may be buying a business and view the earn-out structure as protection against paying today for future performance that may never happen.

The problem is that an earn-out often depends on what happens after control shifts. Once the deal closes, the buyer may control the acquired business, customer relationships, employees, pricing, records, accounting procedures, and daily operations that affect whether the business reaches the earn-out targets.

That issue matters even more in an asset purchase agreement. The buyer may not keep the acquired business separate during the earn-out period. It may move customers into its own systems, reassign key employees, bundle services, change pricing, or allocate expenses in ways that affect the calculation and any later payment.

This article explains how earn-out provisions work in asset purchase agreements, why they can lead to post-closing disputes, and which terms New Jersey and New York business owners should review before treating an earn-out as real purchase price.

Quick Answer: What Is an Earn-Out Provision in an Asset Purchase Agreement?

An earn-out provision in anasset purchase agreement makes part of the purchase price depend on future performance after closing. Instead of paying the entire price up front, the buyer agrees to make additional earn-out payments if the acquired business,acquired assets, customer accounts, or other agreed business activity reaches defined performance targets during the earn-out period.

In an asset purchase deal, the important issue is not only whether the business meets the earn-out targets. The earn-out structure should also explain what business activity counts, how the earn-out will be calculated, who controls the records and post-closing operations, and how the seller can challenge the buyer’s calculation if the parties disagree.

How Earn-Outs Work in Asset Purchase Agreements

The Buyer Pays a Closing Amount

In most asset deals, you receive a closing payment when the deal closes. That payment is the fixed part of the purchase price, subject to any adjustments the asset purchase agreement requires for debt, working capital, unpaid expenses, or similar closing items.

The earn-out is different. It is contingent consideration, which means the buyer may owe it later only if the acquired business reaches the agreed performance targets during the earn-out period. You should read the purchase price as two separate pieces: the money paid at closing and the potential earn-out payments tied to future performance.

The Asset Purchase Agreement Creates a Possible Later Payment

The earn-out provision creates a possible later payment, not an automatic one. If you own or are buying a New Jersey or New York business, the asset purchase agreement should give a clear test for when future earn-out payments become payable.

Read the earn-out target from your side of the deal:

If you are selling, identify the exact earn-out targets that must be met before the buyer owes payment.

If you are buying, confirm that the targets reflect future performance you are willing to pay for after closing.

The important point is that the earn-out terms should define the performance metrics clearly enough to support an earn-out calculation after closing.

The Asset Purchase Agreement Defines the Earn-Out Period

The earn-out period is the window used to measure future performance after closing. You should know when that window starts, when it ends, and whether the earn-out structure divides it into separate calculation periods.

The table below breaks down the timing terms that can affect how the earn-out period works and what happens if a target is missed.

Timing Issue

What It Means for You

Start date

The date the earn-out clock begins, such as the closing date or another agreed date.

End date

The date the buyer stops measuring performance for earn-out purposes.

Separate calculation periods

Different testing windows, such as a short earn-out period followed by a later measurement period.

Missed-period treatment

Whether missing one target affects only that period or also affects future earn-out payments.

This matters because each calculation period may be tested separately. If the acquired business misses the first performance target but reaches a later earn-out target, the purchase agreement should say whether the seller can still receive the later earn-out amount.

The Asset Purchase Agreement Chooses the Metric

The earn-out metric is the test used to decide whether future performance supports another payment. It should match what the buyer is actually acquiring and what both sides can measure after closing.

Different performance metrics shift risk in different ways:

A revenue-based earn-out may be easier to follow, but the agreement should say which customer accounts, contracts, products, or services count after closing.

An EBITDA-based earn-out focuses more on operating performance, but you need to review which expenses, overhead charges, and buyer allocations can reduce the earn-out calculation.

A milestone-based earn-out may work when payment depends on a defined event, such as customer retention, a sales target, or regulatory approval. The milestone should be objective enough to support a later determination.

In an asset purchase deal, the metric should connect to the acquired business activity being sold. If the buyer later folds the assets into its post-closing operations, unclear earn-out metrics can make potential earn-out payments harder to verify.

The Formula Turns Performance Into Money

Once your asset purchase agreement chooses the earn-out metric, the formula decides how the measured result becomes an earn-out amount. It should tell you when any earn-out payments begin and whether performance below the maximum target still produces money.

The formula may use a threshold, a payment range, a cap, or a full earn-out trigger. Do not judge the earn-out by the highest possible number. The formula determines whether near-miss financial performance earns a partial payment or nothing.

The threshold tells you the minimum performance target before any earn-out payment begins.

A partial-payment range tells you whether the acquired business can miss the upper target but still produce some payment.

The cap tells you the most the buyer must pay, even if future performance exceeds the agreed target.

The full earn-out trigger tells you when the maximum earn-out amount becomes payable under the asset purchase agreement.

Example: Assume the earn-out starts once EBITDA reaches $2 million, pays proportionally between $2 million and $2.5 million of EBITDA, and is capped at $1 million. If post-closing EBITDA reaches $2.3 million, the business has achieved $300,000 of the $500,000 EBITDA range between the threshold and the full earn-out trigger. That equals 60% of the range, which would produce a $600,000 earn-out payment. If EBITDA reaches $2.5 million or more, the buyer would owe the full $1 million. If EBITDA reaches only $1.9 million, no earn-out payment is owed.

The Buyer Calculates the Earn-Out After the Period Ends

After the earn-out period closes, the buyer usually prepares the first earn-out calculation. That makes sense because the buyer now controls the acquired business, the accounting systems, and the records used to apply the formula.

The purchase agreement should require more than a bare number. The earn-out calculation statement should show the performance metric applied, the period covered, the accounting procedures used, and the earn-out amount the buyer says is owed.

If you are selling, this report helps you test the buyer’s math. If you are buying, a clear reporting process can reduce post-closing disputes by showing what must be delivered after the earn-out period ends.

The Seller Gets a Limited Time to Review and Object

After the buyer sends the earn-out calculation statement, your asset purchase agreement should give you a defined review period. That deadline may matter as much as the earn-out formula itself.

During the review period, you should be able to check the records supporting the performance metric, the accounting procedures used, and the earn-out amount the buyer says is owed. The agreement should also explain what your objection notice must include.

A clear objection process protects both sides. It gives the seller a real opportunity to challenge the calculation, while helping the buyer move the earn-out process toward finality instead of leaving every number open to dispute.

If you do not object on time as the seller, the buyer’s calculation may become final under the asset purchase agreement. Treat the review period as a real deadline, not a routine update from the buyer.

Disputes Usually Go to an Accountant or Auditor

When you object to the buyer’s earn-out calculation and cannot resolve the disagreement, your asset purchase agreement may send the disputed items to an independent accounting firm or auditor. That process usually addresses the numbers, not the entire deal.

You should:

Know which disputed items the accountant is allowed to review.

Check whether the accountant must follow the earn-out formula, performance metric, and accounting procedures already written into the purchase agreement.

Not assume the accountant can fix vague earn-out terms after closing.

Confirm whether the accountant’s decision becomes the final determination of the earn-out amount.

The key point is simple: the accountant should apply the earn-out terms, not rewrite them after closing. Clear drafting before a dispute begins helps prevent a narrow accounting disagreement from becoming broader litigation.

Common Areas That Cause Earn-Out Disputes

Once you understand the earn-out process, the next issue is where it can break down. You are better off identifying likely earn-out disputes before signing than trying to fix unclear terms after closing.

Issue 1: The Agreement Is Unclear About How Much Can Actually Be Earned

You may see a deal described as “$4 million plus up to a $1 million earn-out” and think of the deal as a possible $5 million sale. The asset purchase agreement may tell a more limited story.

The cap may control your upside. A cap is the ceiling on the earn-out amount. If the acquired business performs better than expected, you may stop sharing in that upside once the cap is reached. For the buyer, the cap can make the purchase price exposure more predictable.

The minimum payment may control your downside. A minimum payment gives the seller some protection if the acquired business does not fully hit the performance target. A buyer may resist that term because an earn-out is usually meant to pay only for agreed future performance.

An all-or-nothing formula creates near-miss risk. Some earn-out provisions pay nothing unless the target is fully met. If the business gets close but misses, the seller may receive no earn-out payments for that period.

A partial-payment formula can reduce cliff risk. The purchase agreement may provide no payment below a lower target, partial payment within a stated range, and a full earn-out only at the upper target. That kind of earn-out structure makes close performance matter.

For example, an all-or-nothing earn-out tied to $10 million in revenue may pay nothing if revenue reaches $9.99 million. A partial-payment structure could treat that near miss differently, such as paying part of the earn-out once revenue passes $9.5 million and paying the full amount at $10 million.

Issue 2: The Business Performs Unevenly After the Sale

A business rarely performs in a straight line after closing. Your business may have a slower transition, then improve once customers settle, key employees adjust, or the buyer’s systems begin working.

The earn-out period can help you, hurt you, or cut off payment eligibility before the acquired business has enough time to perform. That is why timing language matters as much as the earn-out targets themselves.

A short earn-out period can give faster certainty. You may find out sooner whether the buyer owes any earn-out payments. The downside is that a short earn-out period may not give the acquired business enough time to stabilize after closing.

A longer earn-out period can better reflect post-closing business performance. It may give the company more time to adjust, especially if customers or systems need a transition period. It also keeps buyers and sellers tied to the earn-out structure longer, which may create more room for disputes.

Missed earn-out periods need clear treatment. If the business misses the Year 1 target but hits the Year 2 target, your purchase agreement should say what happens next. The following could happen:

The Year 1 earn-out may be lost forever.

The Year 2 earn-out may still be paid, while Year 1 remains unpaid.

Strong Year 2 performance may make up for part of the missed Year 1 earn-out amount.

A cumulative target may apply across the full earn-out period.

For example, assume the earn-out pays $500,000 for each year the business reaches $1 million in EBITDA. If the business reaches $900,000 in Year 1 and $1.2 million in Year 2, the result depends on the agreement. If each year stands alone, the seller may receive only the Year 2 payment. If the agreement uses a cumulative $2 million target across both years, the seller may receive the full $1 million because total EBITDA reached $2.1 million.

Clawbacks and catch-ups decide whether periods are final. A clawback may let the buyer recover earn-out payments made earlier if later performance falls short. A catch-up may let later strong performance make up for an earlier missed target.

This kind of timing issue can change the practical purchase price. If you are selling, check whether an early miss could permanently reduce your payment. If you are buying, check whether later financial performance can affect an earlier period.

Issue 3: The Buyer’s Post-Closing Conduct Affects Whether the Earn-Out Target Is Reached

After closing, the buyer may control the acquired business while you are still waiting for earn-out payments. That is the central tension. Decisions about staffing, customer handling, pricing, records, and integration can affect whether the earn-out targets are reached.

The agreement should balance the buyer’s need to operate the purchased assets with the seller’s need for protection against decisions that could make the earn-out harder to achieve or verify.

Your asset purchase agreement can address that tension through post-closing covenants, including:

Separate books and records, so you can still track the acquired business during the earn-out period.

Restrictions on diverting customers or resources, so the buyer does not move revenue or support away from the earn-out calculation.

Key employee provisions, if your earn-out depends on specific people remaining involved after closing.

Good faith or commercially reasonable efforts language, so the buyer has operating flexibility but cannot use arbitrary or unreasonable conduct to reduce or avoid future earn-out payments.

The buyer may want language saying it has no obligation to maximize the earn-out. That can be reasonable, but your agreement should still say whether the buyer’s management has full discretion or whether post-closing covenants protect the earn-out structure.

Issue 4: The Seller Cannot Verify the Buyer’s Calculation

You may believe the earn-out was earned, but belief is not enough. If the buyer gives you only a final number, you may not be able to tell whether the right revenue, customer accounts, expenses, or adjustments were included.

Your agreement should give you access to the backup records needed to review the number, including:

Records supporting the performance metric.

Separate books or tracking for the acquired business, if the earn-out depends on that business remaining identifiable.

The accounting procedures used to calculate revenue, EBITDA, or another financial metric.

Any adjustments that changed the earn-out amount.

Clear record-access rules protect the seller’s ability to challenge the calculation before the deadline expires while helping the buyer keep any dispute focused on specific calculation issues.

Issue 5: The Payment Is Earned but Reduced, Delayed, or Redirected

Even if the earn-out target is met, the payment may not arrive in full. Your asset purchase agreement may allow the buyer to reduce the earn-out amount, hold back part of the payment, or place funds in escrow while another claim is unresolved.

Offset rights are usually the first place to look. If the buyer claims the seller owes money under the purchase agreement, the buyer may try to subtract that amount from future earn-out payments.

Your agreement should address the payment mechanics clearly:

Offset rights may let the buyer subtract sellerliabilities from the earn-out payment.

Holdbacks may let the buyer keep part of the payment until a claim is resolved.

Escrow provisions may send part of the payment to a third-party account instead of directly to the seller.

Interest provisions decide whether late or withheld payments grow while the dispute is pending.

Security for earn-out payments may include aparent guaranty, letter of credit, escrow, or another source of payment protection.

If you are selling, do not stop once the earn-out amount is calculated. Check whether another provision can reduce, delay, or redirect payment. If you are buying, define those rights clearly so they address real claims without creating unnecessary post-closing disputes.

Issue 6: The Buyer Sells, Restructures, or Exits Before the Earn-Out Period Ends

The earn-out period may last months or years after closing. During that time, the buyer maysell the acquired business, transfer assets to an affiliate, merge operations, or restructure the business line being measured.

Those changes create a practical tension. The seller may need the earn-out to remain measurable, while the buyer may need room to sell, reorganize, or integrate the acquired business without automatically triggering the full earn-out.

Your asset purchase agreement can deal with that risk in several ways:

Acceleration may make some or all remaining potential earn-out payments due after a sale, liquidation, or transfer.

Third-party assumption may require the new owner to take over the remaining earn-out obligation.

Buyer remaining liable may prevent the original buyer from being released after a transfer.

A buyout option may let the buyer end the earn-out early by paying a stated amount.

If the earn-out period extends beyond closing, do not leave this issue unstated. The agreement should say what happens if the acquired business is sold, transferred, liquidated, or reorganized before the earn-out period ends.

Speak to Our New Jersey and New York Business Attorneys Today

At Wilkinson Law LLC, we help New Jersey and New York business owners make sense of deal terms that can quietly change the value of a sale and when payment is made. We advise owners on business, commercial, and transactional matters, including the legal and practical issues that shape how a business is sold, how risk is allocated, and how purchase price terms work in real life.

If an earn-out appears in your asset purchase agreement, we help you understand what it means, where the pressure points are, and what should be addressed before the deal moves forward.

We can help by:

Reviewing the earn-out provision in your asset purchase agreement to identify where the purchase price is fixed and where it remains contingent.

Analyzing the earn-out metrics, payment formula, earn-out period, and accounting procedures to see whether the terms are workable in practice.

Identifying areas where buyer control over post-closing operations could make future earn-out payments harder to achieve or harder to verify.

Helping you assess whether the earn-out fairly bridges a valuation gap or leaves too much of the deal exposed to uncertainty.

Spotting sale-readiness issues that may give the buyer a reason to shift risk back to you, including transferability concerns, weak documentation, and founder dependence.

Helping you raise the right issues before the purchase agreement is treated as nearly final, when your leverage may already be narrowing.

Are you wondering about any of the issues mentioned above? Please email us at info@wilkinsonlawllc.com or call (732) 410-7595 for assistance.

AtWilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthybusiness advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQs

Is an Earn-Out Guaranteed?

No. An earn-out is usually not guaranteed unless the asset purchase agreement says otherwise. It is usually conditional, which means the seller receives earn-out payments only if the acquired business meets the agreed earn-out targets during the earn-out period.

What Is the Difference Between an Earn-Out and Seller Financing?

Seller financing usually means the buyer owes part of the purchase price over time. An earn-out is different because payment depends on future performance. If the performance targets are not met, the seller may receive less than the full earn-out amount.

How Long Should an Earn-Out Period Last?

The right earn-out period depends on what the parties are measuring. A short earn-out period may reduce uncertainty, but it may not give the acquired business enough time to prove performance. A longer period may create more room for disputes.

What Earn-Out Metric Is Best: Revenue, EBITDA, or Some Other Metric?

There is no single best earn-out metric. Revenue may be easier to track, but it may not show profitability. EBITDA or net income may better reflect financial performance, but they usually require clearer accounting procedures.

Can the Buyer Change the Business After Closing?

Usually, yes. After closing, the buyer often controls the acquired business. The asset purchase agreement should say whether the buyer has full discretion or whether post-closing covenants limit changes that could affect the earn-out calculation.

What Happens if the Seller Stays Involved After Closing?

The purchase agreement should say whether the seller’s continued involvement affects the earn-out. If the seller is terminated, resigns, or has a reduced role, the agreement should explain whether future earn-out payments are preserved, reduced, or lost.