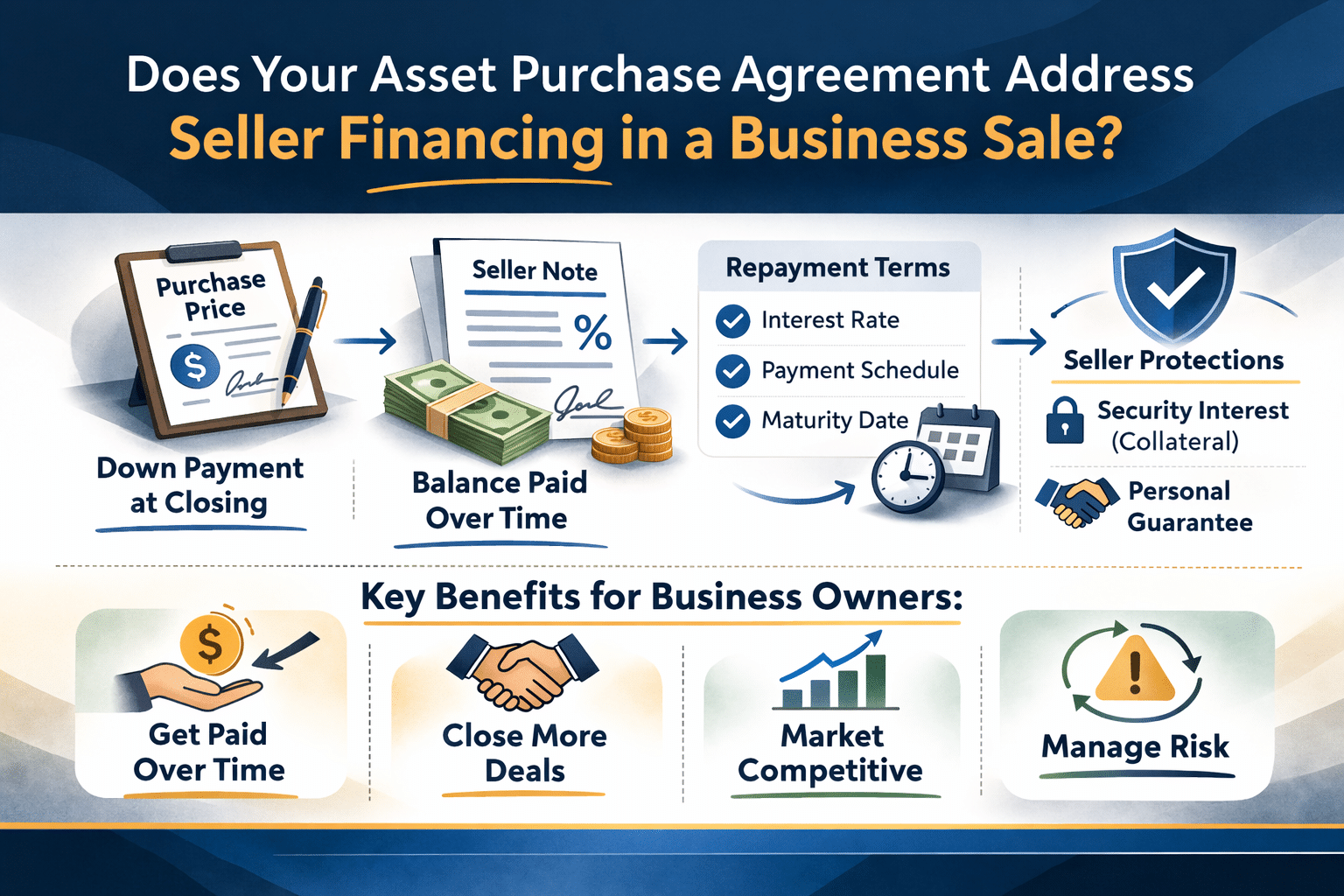

Seller financing in a business sale means you receive part of the purchase price after closing rather than all in cash.

The unpaid balance usually becomes a loan documented in a note, often called a seller promissory note.

The promissory note sets the interest rate, payment schedule, repayment terms, and default provisions that govern how the buyer repays the loan.

Many sellers add additional protections, such as a security agreement or personal guarantee, to reduce the risk of nonpayment.

The interest rate on a seller financing loan must fall within federal tax guidelines and state usury limits.

A well-structured seller financing arrangement can help complete a business sale while helping you manage risk.

You may be considering seller financing in a business sale because your buyer cannot pay the full purchase price at closing. Instead, the buyer asks you to accept part of the payment over time after the business changes hands.

When reviewing a proposed asset sale deal like this, you want to understand the risk before agreeing to it. Questions about repayment, interest rates, collateral, and guarantees often arise once seller financing enters the negotiation.

This article explains how seller financing works in a business sale and what your asset purchase agreement should address, including the down payment, promissory note, repayment terms, security interests, and legal protections that may help you reduce risk.

Join us below for more detail.

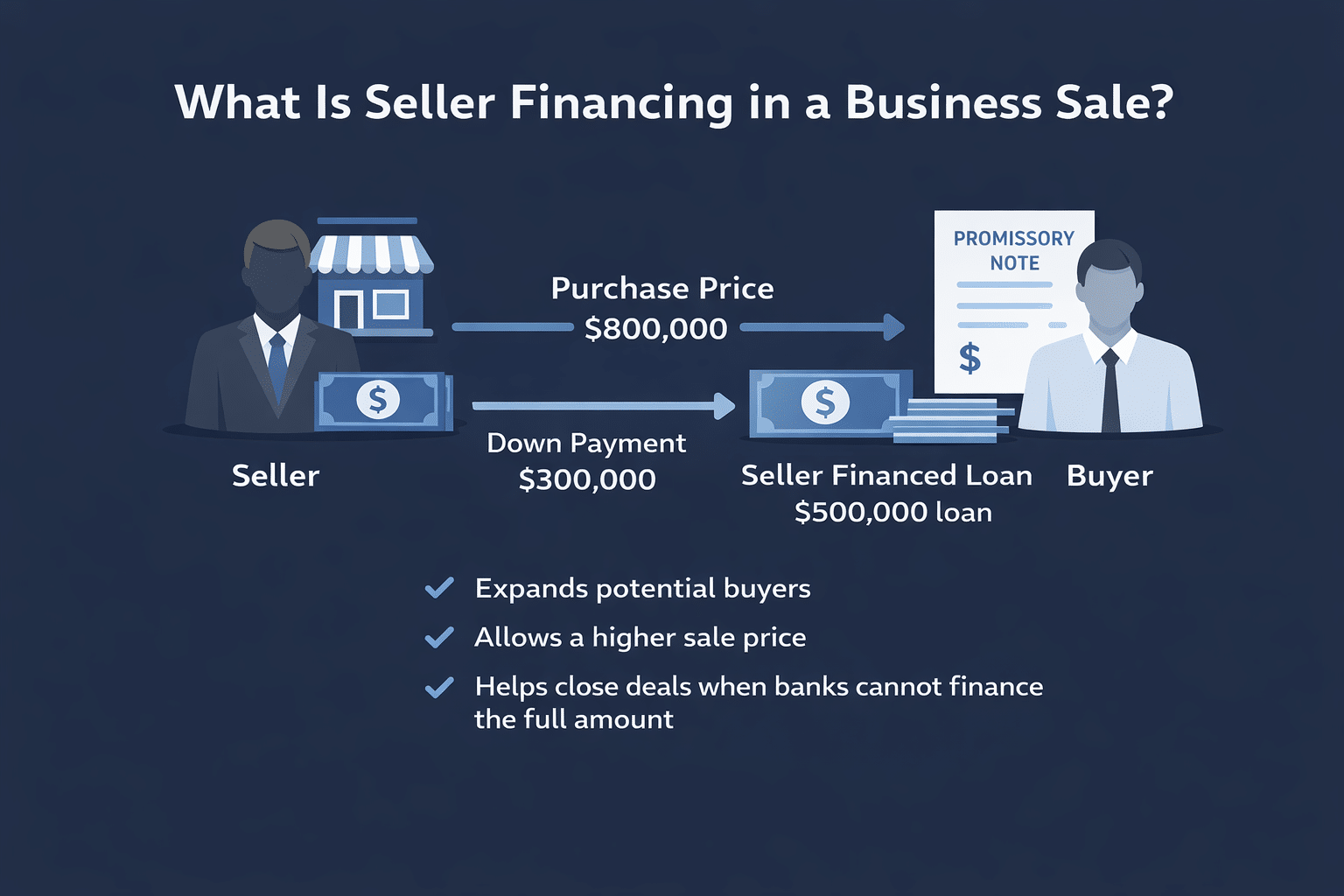

What Is Seller Financing in a Business Sale?

Imagine you are selling your business and the agreed purchase price is $800,000. In the most straightforward scenario, the buyer pays the full amount in cash at closing and the sale is complete. In reality, many buyers cannot fund the entire purchase price without additional financing.

The buyer cannot obtain enough bank financing Banks typically require the buyer to contribute personal capital. A lender may approve only part of the loan needed for the business sale.

Small Business Administration (SBA) loans may require seller participation Many business acquisitions rely on Small Business Administration financing, particularly SBA loans. In some SBA-backed transactions, the lender will not fund the entire purchase price. As a result, the seller may need to agree to receive part of the purchase price over time, effectively financing a portion of the deal instead of being paid in full at closing.

The buyer may need to preserve cash If a buyer spends all available capital on the purchase price, the business may face pressure on cash flow after closing. Seller financing allows some capital to remain available for operations.

The buyer may want to limit risk When part of the purchase price is paid over time, the buyer views the seller as sharing some of the risk associated with the business.

For you as the seller, understanding seller financing becomes essential. In a seller-financed business sale, you agree to accept part of the purchase price later rather than receiving the entire amount in cash at closing. The unpaid balance becomes a loan owed by the buyer.

The example below shows how that structure might look.

How an Asset Purchase Agreement Structures Seller Financing

Now that you understand what seller financing is and what the buyer is asking of you as the seller, it helps to look at how this type of financing usually appears in an asset purchase agreement.

In a typical business sale, the agreement refers to the financing structure, but the details of the loan appear in separate documents. The structure of the deal usually unfolds as follows:

The buyer pays a down payment in cash at closing. This initial payment reduces the remaining purchase price and confirms that the buyer has committed capital to the transaction.

The unpaid balance of the purchase price is documented in a promissory note. In many transactions, this document is also called a seller note because the seller becomes the lender for that portion of the deal.

The buyer repays the remaining balance over time. Payments follow the repayment terms set out in the promissory note and usually include interest on the outstanding loan.

The promissory note plays an important role in a seller-financed business sale. We will look at it more closely below.

Why the Promissory Note Matters

When you agree to seller financing in a business sale, the promissory note becomes one of the central documents in the deal. It is the written agreement in which the buyer formally promises to repay the unpaid portion of the purchase price.

You can think of the promissory note as the debt document for the transaction. Once the sale closes and the buyer takes control of the business, the remaining balance of the purchase price becomes a loan owed to you as the seller.

The promissory note usually sets out the specific financial terms that govern how the buyer will repay the loan. These details typically include:

The principal amount owed under the seller note.

The interest rate applied to the outstanding balance.

The repayment terms that describe how long the buyer has to repay the loan.

The payment schedule showing when each payment must be made.

The maturity date when the remaining balance must be paid.

Default provisions that describe what happens if the buyer fails to pay.

Late charges, if the agreement allows them.

Prepayment rights, if the buyer is allowed to pay the loan earlier than scheduled.

Your asset purchase agreement may state that the buyer will pay the remaining purchase price over several years. That statement alone does not create a detailed loan obligation. The promissory note converts that general promise into a specific legal commitment that governs payment, interest, and enforcement.

That is why the promissory note carries so much weight in a seller-financed business sale.

Key Terms in a Seller Financing Promissory Note

Term

What It Means for You as the Seller

Principal amount owed under the seller note

This is the portion of the purchase price that the buyer did not pay in cash at closing. It becomes the loan balance that the buyer must repay to you over time under the seller note.

Interest rate applied to the outstanding balance

The interest rate determines how much the buyer pays for the use of your money. Interest accrues on the remaining balance of the loan until the loan is fully repaid.

Repayment terms

These terms describe how long the buyer has to repay the loan. In many seller financing business sale transactions, repayment may occur over several years according to the terms set out in the promissory note.

Payment schedule

The payment schedule explains when payments must be made. Many seller financing arrangements require monthly payments, although other schedules may be used depending on the structure of the deal.

Maturity date

The maturity date is the final deadline for repayment. If any balance remains unpaid at that time, the buyer must pay the remaining amount in full.

Default provisions

Default provisions describe what happens if the buyer fails to make a required payment or violates another term of the promissory note. These provisions outline the remedies available to the seller.

Late charges

Some promissory notes allow the seller to charge an additional fee when a payment is made after the due date. Late charges are intended to encourage timely payment.

Prepayment rights

Prepayment rights explain whether the buyer can repay the loan early. Some agreements allow early repayment without penalty, while others place limits on prepayment.

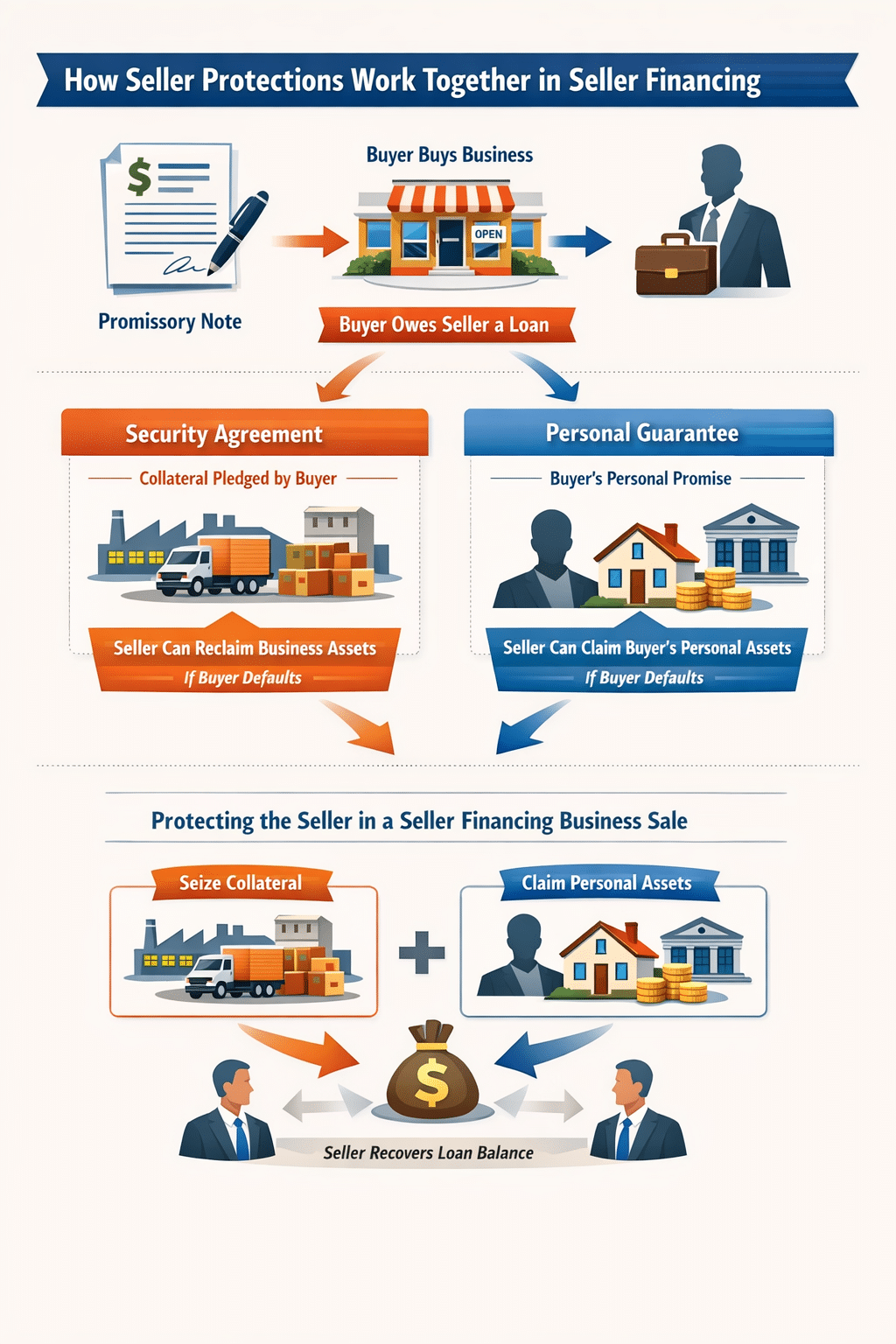

Additional Protections for the Seller in a Seller Financing Business Sale

The promissory note creates the buyer’s obligation to repay the remaining purchase price.

If you agree to seller financing in a business sale, that unpaid portion of the purchase price becomes a loan that the buyer must pay to you over time. Because of that structure, many business sellers look for additional protections in case the buyer fails to make the required payments.

Two commonly used protections address that concern in different ways.

Security agreements, which give you rights in collateral connected to the business.

Personal guarantees, which make the buyer personally responsible for the remaining debt.

Each protection serves a different purpose in a seller financing structure.

Security Agreement

A security agreement allows you, as the seller, to obtain a security interest in specified assets connected to the business. Those assets serve as collateral for the unpaid portion of the purchase price.

Under this arrangement, the buyer pledges certain property to secure repayment of the seller note. If the buyer fails to make payments required under the promissory note, you may have the legal right to repossess or sell that collateral in order to recover the remaining loan balance.

What Collateral Usually Includes

In many seller financing transactions involving a business sale, the collateral includes the same assets that transferred to the buyer as part of the transaction.

Examples may include:

Equipment used in the business

Inventory held by the company

Accounts receivable generated by the business

Furniture and fixtures used in operations

Trademarks or other intellectual property associated with the business

Because you previously owned these assets before the sale closed, using them as collateral often serves as a practical safeguard. If the buyer stops making payments on the promissory note, you may have the right to reclaim or sell those assets in order to recover the unpaid balance of the purchase price.

Perfecting the Security Interest (UCC Filing)

The security agreement establishes your claim against the collateral. To strengthen that claim, you typically file a UCC-1 financing statement, commonly referred to as a UCC filing.

The UCC filing performs several important functions:

It publicly records your claim against the collateral

It establishes your priority relative to other lenders

It helps protect your position if the buyer later borrows money from a bank

Without a UCC filing, another lender could potentially obtain a stronger claim against the same collateral.

For that reason, security agreements in seller financing transactions are commonly paired with a UCC filing shortly after closing the business sale.

Personal Guarantee

A personal guarantee protects you from a different risk that can arise in a seller-financed business sale. Instead of relying on collateral connected to the business, the personal guarantee makes the individual buyer responsible for repaying the loan created by the promissory note.

This issue often appears when the buyer acquires the business through a legal entity such as an LLC or corporation.

If the buyer defaults and the business cannot repay the loan, you may pursue the guarantor’s personal assets in order to recover the remaining balance owed under the seller financing arrangement.

Those assets might include:

Personal bank accounts

Investment accounts

Real estate owned by the guarantor

The personal guarantee prevents the buyer from relying entirely on the corporate structure to avoid responsibility for the loan.

Interest Rates, Taxes, and Legal Limits

When you finance part of a business sale, the interest rate on that loan is not simply a business term negotiated between you and the buyer. It can also affect the tax treatment of the transaction and must comply with state law.

You can think of the interest rate in a seller-financed business sale as operating within two boundaries.

Minimum Interest Rate

At the lower end, the rate cannot fall too far below market levels without creating potential federal tax issues. The Internal Revenue Service (IRS) publishes monthly Applicable Federal Rates, commonly referred to as AFRs, for use in federal tax rules involving loans and other debt instruments.

If the interest on a seller note is set too low, the IRS may view part of the transaction differently for tax purposes. That adjustment can affect the tax burden associated with the deal, including how interest and capital gains tax may be treated.

Maximum Interest Rate

At the upper end, interest rates cannot exceed the limits imposed by state usury laws. These laws restrict the maximum interest that a lender may charge on a loan. In a seller-financed business sale, the seller effectively becomes the lender for the unpaid portion of the purchase price, which means the agreed interest rate must fall within the legal limits established by the state governing the transaction.

Before You Agree to Seller Financing in a Business Sale: A Practical Checklist

The questions below can help you review the deal more carefully before signing the asset purchase agreement.

Does the asset purchase agreement clearly state the down payment due at closing? The agreement should identify the cash amount the buyer will pay at closing and how that payment reduces the remaining purchase price.

Does the promissory note clearly state the amount owed? The note should specify the principal balance that the buyer must repay after closing.

Are the interest rate and repayment terms written into the promissory note? The document should explain how interest will be calculated and how long the buyer has to repay the loan created by the seller financing.

Does the promissory note include a clear payment schedule? You should know when payments are due and how the buyer will repay the remaining balance over time.

Are default provisions defined if the buyer fails to make payments? The note should explain what happens if the buyer misses a payment or violates another obligation under the loan.

Is a security agreement included to protect your position as the seller? A security agreement may give you a security interest in business assets that transferred in the sale, creating collateral for the seller note.

Has a UCC filing been prepared to record the security interest? Filing a UCC-1 financing statement publicly records your claim against the collateral and helps establish priority relative to other lenders.

Does the buyer provide a personal guarantee? If the buyer purchases the business through an LLC or corporation, a personal guarantee may allow you to pursue the individual buyer if the business cannot repay the loan.

Reviewing these points before closing can help you understand how the seller financing portion of the deal is structured and what protections exist if the buyer does not repay the remaining purchase price.

Speak to Our Business Attorneys Today

Seller financing can help you complete a business sale when the buyer cannot pay the full purchase price at closing. When structured carefully, it can move the deal forward while helping you manage repayment risk.

Our business attorneys can help you structure seller financing terms, review your asset purchase agreement, and document promissory notes, collateral, and guarantees so the transaction reflects your goals and risk tolerance.

Are you wondering about any of the issues mentioned above? Please email us at info@wilkinsonlawllc.com or call (732) 410-7595 for assistance.

At Wilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthy business advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQ

How Much of the Purchase Price Do Sellers Usually Finance?

Seller financing often covers a portion of the purchase price rather than the entire amount. In many business sales, the buyer pays a down payment at closing, and the seller finances the remaining balance through a seller note.

The percentage can vary widely depending on the transaction, the buyer’s financial position, and whether bank financing or SBA loans are involved.

What Happens if the Buyer Sells the Business Before the Seller Note Is Repaid?

Many seller financing arrangements address this risk directly in the promissory note or related agreements.

Some notes require the remaining balance to be paid in full if the buyer transfers ownership of the business. Others allow the loan to remain in place if the seller approves the new owner.

Can a Bank Still Lend Money to the Buyer if the Seller Is Financing Part of the Deal?

Yes, many business acquisitions combine bank financing with seller financing.

In those situations, the bank may require the seller note to be subordinated to the bank loan. This means the bank’s loan is repaid before the seller receives payments if financial problems arise.