Menu

Profits Interests in LLCs Taxed as Partnerships: How They Work as Incentive Compensation

April 18th, 2023

Contributor: Anthony Wilkinson

Key Points for Business Owners

- A profits interest can reward future growth without giving away current company value.

- A profits interest is not the same as a capital interest.

- The tax appeal depends on careful structure.

- The Section 83(b) election can materially affect the outcome.

- The documents need to match the deal you think you are making.

If you run a New Jersey LLC taxed as a partnership, you may want to reward a key contributor without giving away current company value.

A profits interest can give that person a stake in future profits and growth without giving them a share of the company’s current liquidation value.

Before you issue profits interests, you need to understand fair market value, tax treatment, the Section 83(b) election, and the operating agreement terms that will shape the holder’s rights.

What Is a Profits Interest in an LLC Taxed as a Partnership?

A profits interest is a form of equity compensation used by many limited liability companies taxed as partnerships. It gives a key contributor a partnership interest tied to future value.

The profits interest holder shares in future profits and future appreciation after the grant date. In that sense, the interest can function like an ownership interest in the company's later growth.

It usually does not give the holder the company’s current liquidation value on the grant date. That is why a profits interest differs from a capital interest and preserves existing value.

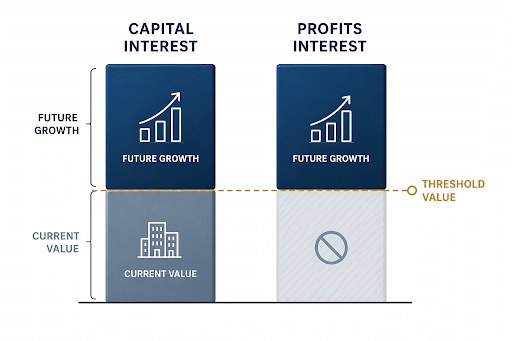

How a Profits Interest Differs From a Capital Interest

A capital interest gives the holder a share of the company’s current value. A profits interest works differently. It only lets the holder participate above a threshold value, usually tied to fair market value on the grant date. That is why a profits interest represents future appreciation rather than existing company wealth.

If the LLC had an immediate liquidation on the grant date, the profits interest holder would generally receive nothing. A capital interest holder, by contrast, may have rights to current liquidation value because that interest includes existing partnership assets and current equity value.

| Issue | Profits Interest | Capital Interest |

| Right to current value | Usually no. A profits interest does not usually give the holder rights to the current value of the company on the grant date. | Yes. A capital interest gives value tied to the company’s current value. |

| Right to future growth | Yes. The holder can share in future profits and future appreciation above the threshold value. | Yes. The holder can share in future growth and also in existing value. |

| Liquidation value at grant | Usually zero. In an immediate liquidation on the grant date, the profits interest holder generally gets nothing. | Not zero if the interest reaches the current company value and partnership assets. |

| Common use case | Often used as equity compensation for service providers or key employees in limited liability companies taxed as partnerships. | More often used where the recipient receives an actual ownership interest in existing value. |

| Tax sensitivity | Often structured for favorable tax treatment, but only if the grant is designed carefully. | Can create different tax implications because the holder may receive current value at grant. |

| Need for valuation discipline | High. The LLC needs a defensible fair market value and a clear threshold value at grant. | Also high, especially when current value, capital contribution, and ownership economics must be measured precisely. |

Why Business Owners Use Profits Interests as Incentive Compensation

You may consider a profits interest when you want to incentivize a key contributor, but do not want to transfer current company value. In the right setting, a profits interest plan lets you connect compensation to future growth in the company’s equity.

- Retention without an immediate transfer of current value. A profits interest can help you keep key employees or other service providers invested in the business, while preserving the value of the company that already exists on the grant date.

- Future upside without a buy-in requirement. The recipient can share in future profits and future appreciation without making a capital contribution to acquire current equity value.

- A different structure from stock options. Unlike many stock options, profits interests do not usually require an upfront exercise payment. That can make the arrangement easier to use in an LLC taxed as a partnership.

- More flexible than cash compensation alone. If salary increases or bonus payments are not the best fit, a profits interest may give you another way to reward contribution through future growth rather than immediate cash.

- Stronger alignment with business goals. You can structure a profits interest plan around company performance, a personal performance goal, or continued service over time, depending on what you want the incentive to reward.

How the Tax Treatment of Profits Interests Can Be Attractive

For many business owners, the tax appeal is what puts profits interests on the table in the first place. A properly structured grant may avoid immediate compensation income, which is why lawyers and tax advisors sometimes describe it as a potential tax-free grant for federal income tax purposes.

That result usually traces back to what the recipient is actually receiving on the grant date. If the profits interest holder is not receiving current liquidation value, and instead only gets a right to share in future profits and future appreciation above a threshold value, the grant may not be treated like ordinary income paid in cash or property.

The longer-term attraction is different. If the structure holds and the arrangement is respected, later upside may be taxed at capital gains rates rather than ordinary income rates. For an owner trying to reward a key contributor without using only cash compensation, that difference can matter.

None of this should be treated as automatic. The tax treatment depends on the grant terms, the operating agreement, the valuation work, and whether the arrangement fits the relevant Internal Revenue Service guidance and IRS safe harbor rules.

Why the Section 83(b) Election Often Matters

If your profits interest vests over time, the Section 83(b) election moves from background detail to live issue. Until the interest becomes substantially vested, later growth can change the tax result.

The point of an 83(b) election is to lock in the low or zero value of the profits interest on the grant date for tax purposes. That matters when the grant starts with little or no current liquidation value.

Timing is where business owners can get hurt. If the election is not filed on time, vesting can trigger a taxable event later, after the interest has picked up real value.

Keep these dates in mind:

- Grant date: This is the date that starts the clock. It is also the date whose value the holder is trying to lock in for tax purposes.

- 83(b) election deadline: The election generally must be filed within 30 days after the grant date. A late filing can undo the intended tax result.

- Each vesting date: If no timely election is filed, each later vesting point can become more dangerous because the interest may be worth more by then.

That is why this is not clerical cleanup. A missed Section 83(b) election can push the holder into tax on value that was supposed to stay tied to future upside, which can materially change the result you thought you were granting.

What Happens to the Recipient After Receiving a Profits Interest?

Once you grant a profits interest, the recipient’s position can change in ways that are easy to underestimate. The upside may look attractive, but the tax and reporting consequences can feel very different from ordinary employee compensation.

- The recipient may become a partner for tax purposes. A profits interest holder may be treated as holding a partnership interest rather than staying in the same employee position for tax purposes.

- The recipient may stop being treated like a regular employee in the same way. That shift can affect how the service relationship is handled and how the recipient reports income tax.

- Quarterly estimated taxes may become necessary. Instead of relying on payroll withholding, the recipient may need to pay taxes through quarterly estimated taxes.

- Self-employment taxes may apply. The recipient may face self-employment taxes, which can come as a surprise if the person expected compensation to work like ordinary wages.

- The recipient may receive allocations of partnership income. That means the holder may owe income tax on allocated partnership income, even if the business does not distribute matching cash at the same time.

- The business may need to consider tax distributions. If the recipient must pay taxes on allocated income, tax distributions may help address the cash flow pressure that can follow.

Legal and Operating Agreement Issues Business Owners Need to Address

Before you issue profits interests, the legal documents need to match the economics you think you are granting. A profits interest plan can look simple at the business level, but the operating agreement and related partnership agreement need to define the holder’s rights with precision.

Use this checklist before you issue profits interests:

- Confirm whether the operating agreement needs to be amended. In many LLCs taxed as partnerships, the existing operating agreement does not already authorize profits interest units or define how they fit into the company’s equity structure.

- Define the holder’s rights clearly. The documents should say what ownership interest the holder receives, what economic rights attach to it, and what limits apply from the start.

- Address voting rights directly. Do not assume a profits interest holder will have the same control rights as other owners. The operating agreement should say whether voting rights exist, are limited, or do not apply.

- Set transfer restrictions in writing. If you do not want the holder transferring the interest freely, the agreement should say so clearly and should explain any approval requirements.

- Decide how repurchase rights will work. A forced repurchase or buyback provision may matter if the service relationship ends, if vesting stops, or if the company wants a clear path to reclaim unvested interests.

- Spell out what happens on termination. The documents should address whether vested or unvested profits interest units are forfeited, repurchased, or retained after the recipient leaves.

- Review allocation language and waterfall design. The way the agreement handles partnership allocations, distributions, and waterfall economics can affect whether the profits interest works the way you expect.

- Clarify whether any capital contribution is expected. A profits interest often differs from an interest tied to contributed capital, so the documents should make clear whether the holder must contribute anything to receive or keep the interest.

- Make sure the profits interest terms fit the broader partnership agreement. If the operating agreement says one thing and the partnership agreement suggests another, the mismatch can create confusion or disputes later.

Speak to our NJ and NY Business Attorneys Today

If you are thinking about using a profits interest, Wilkinson Law LLC can help you evaluate whether it fits the business problem you are actually trying to solve. In some cases, a profits interest makes sense. In others, a capital interest, phantom equity arrangement, or cash-based incentive may be the better fit.

Our NJ and NY business attorneys help you shape the documents around it. That can include reviewing and amending the operating agreement, defining the holder’s rights, addressing vesting and repurchase terms, and aligning the grant with the broader partnership agreement.

We also help business owners think through the issues that often create problems later, including valuation, tax treatment, the Section 83(b) election, recipient tax consequences, and whether the economics of the grant match the result the owner actually intends.

Are you wondering about any of the issues mentioned above? Please email us at info@wilkinsonlawllc.com or call (732) 410-7595 for assistance.

At Wilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthy business advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQs

Can a Profits Interest Be Granted to Someone Who Is Not Already an Owner?

Yes. A business can grant a profits interest to a senior hire, operator, or other key contributor who is not already an owner. Once granted, that person may hold a partnership interest tied to future profits and future appreciation.

Can a Profits Interest Be Forfeited if the Recipient Leaves the Business?

Yes, a profits interest can be forfeited or repurchased if the recipient leaves, depending on the operating agreement and grant terms. That is why termination treatment, vesting, and any forced repurchase rights should be addressed clearly at the outset.

Does a Profits Interest Always Give the Recipient Voting Rights?

No. A profits interest does not automatically give the holder voting rights. The operating agreement should state whether the profits interest holder has control rights, limited rights, or only an economic ownership interest tied to future growth.

Can a Profits Interest Be Structured So the Holder Shares in Upside but Has Limited Control?

Yes. A profits interest can be structured so the holder shares in future profits and future appreciation while having limited control. That often depends on how the operating agreement defines voting rights, transfer restrictions, and other rights tied to the interest.

What Happens to a Profits Interest if the Company Is Sold?

If the company is sold, the treatment of a profits interest depends on the operating agreement, the waterfall, and the sale terms. A profits interest holder may share in sale proceeds above the threshold value, but the documents control.