Menu

Estate Planning for New Jersey Business Owners: What Happens to Your Business and Wealth After a Sale

April 22nd, 2026

Contributor: Anthony Wilkinson

Key Points for New Jersey Business Owners

- Sold the business? Your old estate plan may no longer fit.

- “It will all go to the family” is not a full plan.

- A will alone may not be enough after a sale.

- Bigger numbers create bigger planning mistakes.

- Partial updates can still leave your family stuck.

- Good planning makes things easier on the people closest to you.

When Business Value Turns Into a Personal Planning Problem

You may have spent years building a business that depends on you more than you like to admit. You know the accounts, the people, the pressure points, and the cost of a bad decision. What often gets less attention is what happens to that value once it stops being tied only to the next month of operations.

That question tends to show up later than it should. Sometimes it shows up after a sale. Sometimes it shows up after a health scare, a conversation at home, or a point where the business is worth enough that “we will figure it out later” stops feeling like a serious plan.

If you are a New Jersey business owner who has created something meaningful and has not fully thought through what happens to it if something happens to you, this article is for you. We will walk through how estate planning for business owners comes up in real life, where the weak spots usually are, and what good planning helps prevent.

To see how this planning gap tends to show up, it helps to start with a New Jersey business owner whose situation is more common than it may sound.

Mike had built a real company, sold it for cash, and only then realized the hard part was not entirely over.

The example below reflects the kinds of planning issues we often see arise for business owners, but it does not represent any specific client matter.

Mike’s Story: A $1M Sale and the Realization That Estate Planning Still Matters

When Mike Delaney sold his HVAC company, he did what a lot of practical business owners would do.

He checked the wire twice, refreshed his banking app once more than he needed to, and then went out to buy himself a sandwich that suddenly felt more expensive than it had the week before.

He had spent twenty-two years building the company. That meant early mornings, summer service calls in older New Jersey homes, payroll weeks that never felt casual, and customers who had his number saved because they trusted him to pick up when the air stopped working in July.

By the time the sale closed, he had sold the business for $1 million in cash. The number was real. So was the relief.

For the first couple of days, Mike felt like the hard part was over. Then the questions started showing up in places he had not expected.

- His wife asked what would happen if something happened to him now.

- His daughter wanted to know whether the money was actually protected or just sitting in an account.

- His son asked whether this changed anything about the family’s plans for the future.

Mike found himself awake later than usual, realizing that “it will go to the family” was not much of a plan once the business had turned into cash. He had handled the sale, but he had not really thought through what estate planning looks like after selling a business, or how those proceeds would be managed if something happened to him.

A friend told him he should talk to a New Jersey trust and estate attorney. Mike’s first reaction was that he had already done the difficult legal work. He had sold the business.

What else was there to figure out? The answer, it turned out, was quite a bit.

The attorney he met with did not treat him like a private wealth client with a sprawling estate. She treated him like what he was: a normal owner who had spent years building something valuable and had not yet lined up the planning around what that value had become after the sale.

She helped him update his will, put basic trust planning in place, clean up beneficiary designations, and sign powers of attorney, a living will, and related health care documents.

She also helped him think through how his personal and business assets had changed after the sale, what would happen if he became incapacitated, and how the money would be managed without leaving his family members to sort it out under pressure.

Mike left with a binder, a plan, and the feeling that he had finally dealt with a problem he had been able to postpone only because nothing had forced him to face it sooner.

Building the business had created the value. The estate planning that followed helped protect what that value was meant to support.

Why Even a $1M Sale Requires a Business Estate Plan

What changed for Mike was not just the number in his account. It was the nature of the planning problem he now faced, one that many New Jersey business owners do not fully see until after a sale or other liquidity event.

Before the sale, most of his attention was fixed on running the company. After the sale, the central question became what would happen to that value, and to any remaining business interests, if he became incapacitated or died. That shift is where estate planning for business owners starts to feel less optional and more concrete.

Why This Becomes Visible After a Sale

A sale often exposes planning gaps that were easy to postpone while the business still demanded daily attention:

- The business has turned into cash or other liquid assets.

- Family members begin asking questions that daily operations used to push aside.

- Older estate planning documents may no longer fit the owner’s current financial reality.

- Broad assumptions, such as “it will all go to the family,” start to feel incomplete.

- The issue becomes less about running the company and more about authority, access, coordination, and whether any business debts or related obligations still affect the broader picture.

For many New Jersey small business owners of closely held businesses, this is the point when a business estate plan becomes important. The business may have sold cleanly, yet the planning around the sale proceeds may still reflect an earlier stage of life. That mismatch is where confusion begins.

What Changed for Mike

| Before the Sale | After the Sale |

| Mike’s focus was on payroll, service calls, and keeping the company moving. | The question became who would have authority if something happened to him. |

| The business was tied to his daily work and cash flow. | The value now sat in personal assets and needed a clear plan. |

| Most decisions were operational. | The issue became how the money would be managed and passed on. |

| Family concerns stayed in the background. | Family members now had immediate questions about protection and clarity. |

Mike did not suddenly become a different person after the closing. What changed was the form of the value he had built and the kind of planning that value required.

What the Attorney Actually Helped Him Do

The trust and estate attorney helped him address practical problems that had become easier to see after the sale, she:

- Updated his will so the baseline plan matched his current life.

- Put basic trust planning in place so the proceeds were not left without structure.

- Cleaned up beneficiary designations so different accounts would not move in conflicting directions.

- Prepared powers of attorney and health care documents so someone could act if Mike became incapacitated.

- Helped connect his personal assets, business assets, and family responsibilities in one workable plan.

That is the part many business owners miss. Estate planning after selling a business is not only about who receives the money at death. It is also about who can step in, what legal documents control, and whether the people closest to the owner would be left with a plan they can actually use for a smoother transition.

Signs This May Apply to You

Mike’s situation may be closer to your own than it first appears if any of the following are true:

- Your current estate planning documents were signed before the business changed materially.

- You sold the business, took a large distribution, or built enough value that the stakes now feel different.

- Your spouse would have trouble locating or understanding key accounts.

- Your planning still rests on general intentions rather than coordinated legal documents.

- You have not reviewed beneficiary designations, powers of attorney, or health care documents in years.

Mike’s story shows why estate planning for NJ business owners is not only a concern for families with much larger balance sheets. It often becomes relevant the moment business value turns into personal wealth.

How Estate Planning for New Jersey Business Owners Changes as Wealth Grows

The next question is what changes when the amount is larger, and the structure needs to do more than simply keep things orderly.

The example below reflects the kinds of planning issues we often see arise for business owners, but it does not represent any specific client matter.

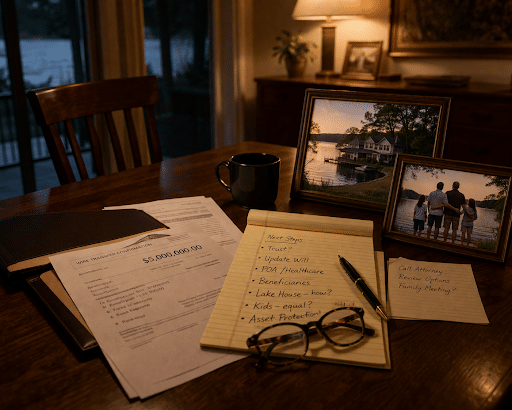

Tom’s Story: When a $5M Sale Requires More Than Basic Estate Planning

On the Friday afternoon the deal closed, Tom Caruso did something he had not done in twenty-three years: he left work while the sun was still up and without anyone calling him on the drive home.

He had sold his industrial supply company for $5 million in cash. After decades of 6:00 a.m. starts, vendor headaches, inventory surprises, and the steady demands that come with running a closely held business, the money was finally real.

Tom celebrated the way many disciplined business owners do. He ordered takeout, opened a decent bottle of wine, and spent half an hour staring at the number on a printed statement like it might vanish if he looked away too long.

By Sunday, the glow had faded.

Then the questions started to change. His wife wanted to know whether the business sale proceeds were just sitting in an account. His son had strong opinions about what should be invested and how. His daughter raised the question of the family lake house, which everyone cared about and no one had ever addressed clearly.

Tom began to see that the issue was no longer simply whether his family members would inherit something. It was whether the same plan made sense for everyone, whether everything should pass outright, and how a larger amount of money could create strain if no one had decided how it was supposed to work.

That was the part he had not planned for.

At $5 million, Tom needed to think about control, timing, and structure. He needed to think about what his wife would need, what his children would be ready to handle, and whether equal treatment would actually lead to a workable result. The larger amount made those estate planning considerations harder to postpone and more important to answer well.

A week later, he met with a trust and estate attorney for business owners. She walked him through the difference between leaving money outright and creating a structure around it. She helped him update his will, put a revocable trust in place, coordinate beneficiary designations, and sign powers of attorney and health care documents.

More importantly, she helped him think through how his personal and business assets should actually flow, who should control what, and how a larger amount of wealth could require more asset protection and a more deliberate plan.

What Tom needed was not just basic estate planning documents. He needed a business estate plan that fit his family dynamics, financial goals, and the realities of a larger liquidity event.

Tom left relieved in a way the sale itself had not managed to provide. The closing had converted his business into money. The planning that followed gave that money structure and made business continuity feel less separate from family protection than it had before.

How Estate Planning for New Jersey Business Owners Evolves With Larger Liquidity Events

Tom’s situation shows that a larger liquidity event does more than increase the amount at stake. It changes the planning problem.

What Changes When the Amount Is Larger

As the number grows, the planning choices become more consequential:

- Vague expectations leave more room for disagreement among family members.

- It matters more whether assets pass outright or stay under some structure.

- Timing becomes more important when beneficiaries are in different stages of life.

- Control matters more when the amount is large enough to affect long-term decision-making.

- Equal treatment does not always lead to a workable result.

A larger amount requires more thought about how wealth should actually work once it reaches the people it is meant to benefit, and how the broader picture works if the business continues in some form after the owner steps back.

What Changes From Mike to Tom

| At Mike’s Level, the Priority Was | At Tom’s Level, the Priority Becomes |

| Making sure the basic estate planning documents were current. | Deciding whether the same plan fits every beneficiary. |

| Coordinating authority and beneficiary designations. | Deciding who should control assets and under what terms. |

| Reducing confusion if something happened suddenly. | Reducing future strain, unclear expectations, or poor timing. |

| Getting the plan to catch up after the sale. | Making the structure match the amount, the family, and the owner’s financial goals. |

The difference is not just the number. Mike mainly needed a business estate plan that caught up to his new reality. Tom needed a business estate plan that could do more work. The issue had moved beyond basic coordination and into questions of structure, control, and how business sale proceeds planning should reflect the actual people involved.

What a Larger Amount Makes Possible, and Risky

A larger amount of wealth gives the owner more planning options, but it also raises the cost of vague planning. That is where estate planning considerations become more layered.

Common pressure points include:

- One child may be financially responsible while another is not.

- A spouse may need support without also needing full control over every asset.

- A family business, second home, or other shared asset may create tension if no one has clarified expectations.

- Outside influence, spending habits, or later life events may matter more once the amount is significant.

- A simple outright transfer may not reflect what the owner actually wants.

This is where questions of asset protection, business continuity, business inheritance planning, business succession planning, and possible estate taxes can start to matter more. A larger amount does not always require a complicated structure, but it does increase the chance that a basic plan will leave important issues unresolved.

What Tom’s Situation Should Make You Think About

Tom’s story is worth attention if any of these questions feel close to home:

- If the amount at stake is larger now, do your current estate planning documents still fit it?

- Would the same distribution approach make sense for each family member?

- Have you thought about who should control assets if the goal is protection, not just transfer?

- Are there family assets or expectations that everyone assumes will work out, but no one has really addressed?

- Does your current plan reflect your financial reality now, or the stage of life you were in before the sale?

If Tom’s situation feels closer to your own, the takeaway is that larger liquidity often creates planning choices that do not show up at lower levels. Those choices are easier to handle when they are made deliberately, before confusion, strain, or avoidable mistakes begin to shape the outcome.

Tom’s situation shows what happens when a business owner recognizes that a larger amount requires more thought and clearer structure. The next problem is what happens when an owner senses that shift, but keeps putting the planning off anyway.

Why New Jersey Business Owners Delay Estate Planning Even When They Know Better

For many New Jersey business owners, this delay does not come from denial so much as momentum. The business keeps demanding attention. Existing documents feel good enough. Nothing is actively on fire. That makes estate planning easy to postpone, even when you already know it deserves a closer look.

| What You May Be Telling Yourself | What May Actually Be Happening |

| “I already have something in place.” | Your current documents may reflect an earlier stage of life or a smaller amount at stake. |

| “We can deal with that later.” | You may be postponing a real planning issue because nothing has forced it into view yet. |

| “My spouse knows what I want.” | General understanding is not the same as legal authority, structure, or coordinated documents. |

| “The sale is done, so the hard part is over.” | The legal problem may have changed rather than disappeared. |

| “Things are simple in our family.” | They may feel simple until money, timing, or uneven expectations put pressure on them. |

You may have enough in place to feel covered, while still missing the coordination, structure, or clarity the situation now requires.

That is why Steve’s story matters. He is not reckless. He is the kind of owner who keeps moving, assumes there is still time, and only sees the weakness in the plan once something happens that makes delay more expensive.

The example below reflects the kinds of planning issues we often see arise for business owners, but it does not represent any specific client matter.

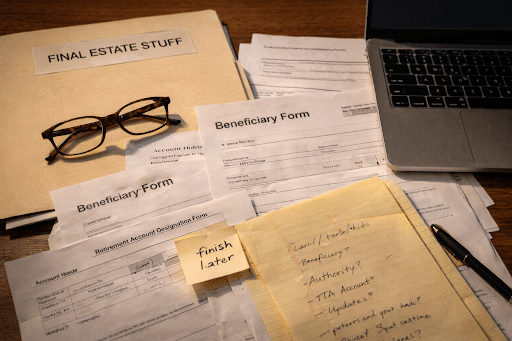

Steve’s Story: What Happens When Estate Planning Keeps Getting Pushed Aside

When Steve Morano sold his specialty signage company for $5 million in cash, he made the same mistake a lot of successful owners make: he assumed that because he had survived twenty years of employees, vendors, clients, insurance renewals, and one forklift incident no one would describe the same way twice, he was now qualified to handle his personal planning by instinct.

His instinct, unfortunately, was not well thought through.

He told his wife, Carol, “If anything happens to me, everything’s simple.” This was comforting in the moment because it was said in a confident voice while holding grilled chicken.

It became less comforting later when Carol asked where the documents were, and Steve said, “Mostly in the office. Or scanned. Somewhere.”

Steve did not meet with a trust and estate attorney. He did, however, rename a folder on his desktop “FINAL ESTATE STUFF,” which gave him a false sense of accomplishment usually associated with buying a treadmill.

That was more or less the pattern. He did enough to feel like he was dealing with it, but not enough to make the plan usable.

He changed one beneficiary designation, forgot three others, left a large account titled only in his own name, and kept telling his adult children that everything would be divided “fair and square,” as though that answered questions about timing, control, or what would happen if Carol needed help managing things first.

It also did not help that one son was responsible, one daughter was responsible-adjacent, and Steve’s brother Nick had already started offering “helpful ideas” about real estate investments involving a marina.

Then Steve had a minor stroke.

He recovered well. The planning did not.

Carol discovered that “simple” meant a stack of half-finished paperwork, accounts that did not line up, conflicting beneficiary designations, and no clear authority for who could do what or when.

Nothing had exploded, exactly. But everything had become slower, costlier, and more stressful than it needed to be. That was the real problem. Steve had not done nothing. He had done just enough to mistake partial action for proper planning.

Common Estate Planning Mistakes New Jersey Business Owners Make After a Sale

Steve’s problem was not that he ignored estate planning altogether. It was that he handled it in fragments and mistook those fragments for a workable plan. That is a common pattern after a sale.

A business owner updates one piece, assumes the rest is close enough, and only later discovers that partial action can leave the family with just enough structure to create confusion.

The mistakes Steve actually made:

- He changed some beneficiary designations and left others untouched.

- He relied on broad assurances instead of coordinated estate planning documents.

- He left at least one significant account titled in a way that no longer matched his situation.

- He assumed his wife and children would be able to fill in the gaps if needed.

- He treated “fair and square” like a plan, even though it did not answer questions about timing, control, or who would manage what.

That pattern matters because it feels responsible while it is happening. A capable owner can make a few updates, organize a folder, mention general intentions to family members, and walk away with the sense that the issue is at least mostly handled.

In reality, estate planning after selling a business often breaks down at the points where no one checked whether the accounts, legal documents, beneficiary designations, and authority to act still point in the same direction.

What Steve’s Situation Should Make You Look At Now

- Are some of your accounts, beneficiary designations, or estate planning documents still tied to an earlier stage of life or business ownership?

- Have you done partial cleanup that made you feel covered without fully reviewing how the whole plan works together?

- Would your spouse know what exists, where it is, and who has the authority to act if you became incapacitated?

- If something happened this year, would your family inherit a workable plan or a series of loose ends?

Steve’s story is useful because it shows how a planning gap can stay hidden while nothing is actively wrong. The business sale may be over. The money may be in the account.

The weak spot is often the assumption that a few updates are enough. In many cases, what matters most is not whether you have started, but whether the plan you have now would actually work for the people who would need it.

What a New Jersey Trust and Estate Attorney Does for Business Owners

Mike needed the basics to catch up. Tom needed more structure. Steve thought partial cleanup was enough. Put together, those stories point to the same question: what does a trust and estate attorney actually help a business owner get right?

| What a Trust and Estate Attorney Can Help You Do | Why It Should Not Be Left to Chance or Piecemeal Updates |

| Review whether your current estate planning documents still fit your assets, family, and current stage of life. | Older documents often reflect a smaller balance sheet or a very different family and business reality. |

| Coordinate beneficiary designations, account structure, and related legal documents. | Partial updates can leave accounts and documents pulling in different directions. |

| Clarify who can act if you become incapacitated. | Good intentions within a family do not create legal authority. |

| Work through whether assets should pass outright or under some form of structure. | A simple transfer plan may not fit every beneficiary or every family situation. |

| Reduce the risk of confusion, delay, and avoidable strain later. | Families often discover the weak spots only when someone actually needs to use the plan. |

| Align the plan with sale proceeds, the owner’s current goals, and the broader wealth strategy. | What felt sufficient before a sale may no longer fit once the numbers change. |

| Identify where the current plan may create avoidable strain, including unnecessary tax burden in some situations. | Owners often focus on transfer alone and miss how structure can affect what the family is left handling later. |

A New Jersey trust and estate attorney helps you leave behind a plan that still makes sense when someone else has to rely on it.

How a New Jersey Trust and Estate Attorney Works With Your Other Advisors

Your trust and estate attorney may be focused on what happens to the money, who has authority, and how the plan works for your family. Even so, that work often depends on decisions that were made somewhere else:

- In the business

- In the sale documents

- In the tax reporting

- In how the proceeds are now being managed

That is why a trust and estate attorney usually works alongside the other advisors already involved.

| Advisor | How the Trust and Estate Attorney Works With Them |

| Business attorney | Reviews ownership documents, sale terms, buy-sell agreements, intellectual property provisions, and other business-side records so the personal plan does not conflict with what was done on the company side. |

| CPA | Coordinates around tax reporting, the business sale, and possible tax liabilities that may affect how the owner wants the plan structured. |

| Financial advisor | Reviews how sale proceeds and other personal assets are being held, invested or managed so the estate plan reflects what actually exists now. |

| Insurance professional | Helps address how insurance affects liquidity, family protection, and tax planning. |

A good trust and estate plan depends on the right people addressing the same reality from their own side, especially when business partners, family members, and personal advisors may all be affected by what happens next.

Speak to Our New Jersey Business Attorneys Today

We work with business owners who have spent years building something meaningful and want the legal and financial pieces to continue making sense after a sale, major distribution, or significant increase in value.

If your current planning still reflects an earlier stage of the business, or if you are no longer sure how the business-side documents, sale proceeds, and personal planning fit together, this may be the right time for a closer review.

Our New Jersey business attorneys can:

- Review business-side documents, ownership history, and sale-related arrangements that may affect broader planning

- Spot issues that should be raised with trust and estate counsel, especially where beneficiary designations, proceeds, ownership structure, or family expectations may no longer align

- Coordinate with trust and estate attorneys, CPAs, financial advisors, insurance professionals, and other advisors involved in the planning process

- Reduce the risk that important business, financial, and legal details will be handled in isolation when a more coordinated approach is needed

If you are dealing with any of the issues discussed in this article, please email us at info@wilkinsonlawllc.com or call (732) 410-7595.

At Wilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthy business advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQs

Do I Need to Revisit My Estate Plan After Selling a Business?

Yes, often. A sale can change the form of your wealth, the people affected by it, and the planning issues that matter. Documents that made sense before the sale may no longer fit what is now at stake.

Is a Will Enough for a Business Owner After a Sale?

Sometimes no. A will may be part of the plan, but it does not answer every question about authority, coordination, beneficiary designations, or how assets should be managed if you become incapacitated or the family situation is more complicated.

How Do I Know Whether My Current Estate Planning Documents Are Out of Date?

A useful sign is whether they reflect your life before the business changed materially. If the business was sold, value increased, family circumstances shifted, or account structures changed, your planning may need a fresh review.

What if My Spouse Already Knows What I Want?

That helps, but it is not the same as a coordinated plan. General understanding does not create legal authority, align beneficiary designations, or answer practical questions about how assets would actually be accessed, managed, or distributed.

When Does a Business Owner Need More Structure, Not Just Basic Documents?

Usually, when the amount at stake is larger, the family situation is uneven, or the owner wants more than a simple, outright transfer. At that point, timing, control, and long-term management often matter more than people expect.

What Happens if a Business Owner Becomes Incapacitated After a Sale?

That depends on what is already in place. If authority is unclear, documents are incomplete, or accounts are not coordinated, a spouse or family member may face unnecessary delay, confusion, and added stress at the worst time.

What Should I Review First if My Business Value or Personal Wealth Has Changed?

Start with whether your estate planning documents, beneficiary designations, account structure, and family intentions still fit together. In many cases, the biggest problem is not one missing document. It is that the pieces no longer line up.

Can a Key Employee Still Matter After I Sell the Business?

Sometimes, yes. A key employee may still matter if transition commitments, deferred arrangements, or business continuity concerns remain part of the broader planning picture after the sale.

Categories: Selling Your Business