If you operate a Limited liability company (LLC) taxed as a partnership and want to reward a key contributor, you may quickly realize there is no simple “equity” model like the one used in corporations. The options exist, but they are not always intuitive.

Each incentive structure affects ownership, control, and tax treatment differently. Choosing the wrong approach can create unintended tax obligations, dilute your interest, or introduce complications that are difficult to unwind later.

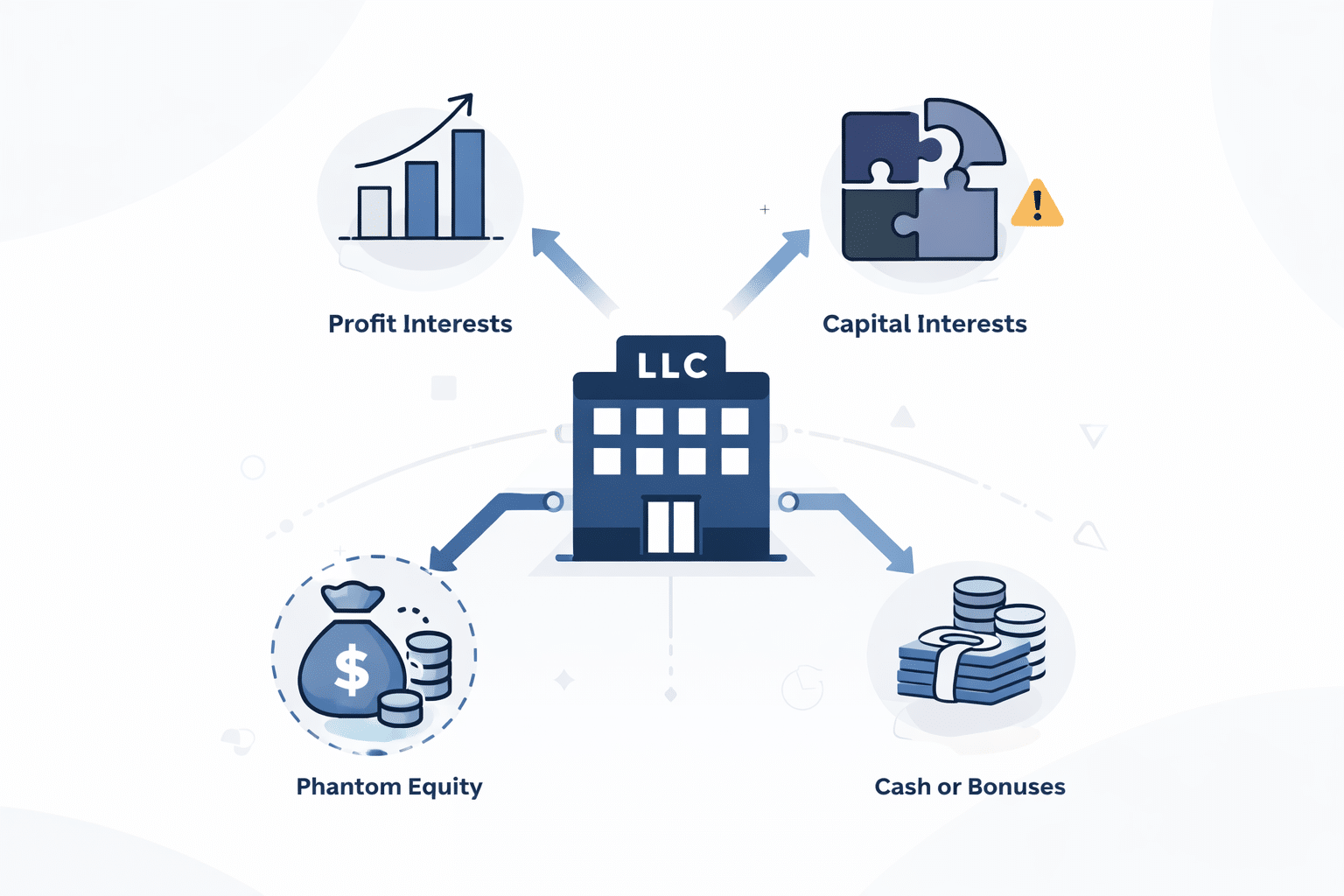

This article explains the main LLC incentive compensation options, including profit interests, capital interests, and phantom equity, so you can see how they differ and begin evaluating which structure fits your situation.

The Big Picture: Types of Incentive Compensation in an LLC

If you are trying to reward someone who matters to your business, the options can feel unclear at first. It helps to know that most LLC incentive compensation options fall into two categories: equity-based compensation and cash-based, including synthetic equity structures.

Equity Incentive Plans

- LLC profit interests: Give the profit interest holder a right to share in future profits without granting current liquidation value in existing LLC assets at the time of the grant.

- Capital interests: Provide an ownership stake in the company’s equity, including current value, which can trigger tax consequences based on fair market value at the time of grant.

- Options on capital interests: Allow a service provider to acquire LLC capital interests at a future date, usually tied to a fixed price and vesting terms.

Cash-Based or Synthetic Compensation

- Phantom equity: Tracks the value of the company’s equity without issuing actual membership interests or changing your ownership percentages. Payments are typically subject to ordinary income tax when paid.

- Performance-based bonuses or guaranteed payments: Provide cash compensation tied to results, typically treated as ordinary income and not connected to LLC ownership.

Each of these approaches affects your ownership, your tax position, and how incentives play out over time.

How These Incentive Compensation Types Compare

Once you see the available structures, the next step is understanding how they differ in practice. The differences show up in ownership, tax timing, and how each arrangement plays out over time.

Seeing these options side by side can make those distinctions clearer:

| Category | Profit Interests | Capital Interests | Phantom Equity |

| Ownership impact | No claim on existing value, tied to future profits | Full ownership stake, including current value | No ownership, no change to LLC membership interests |

| What the recipient gets | Share of future profits and growth | Share of current and future value | Cash tied to company performance or valuation |

| Tax timing | Often no immediate tax if properly structured | Taxable at grant based on the fair market value | Taxed as compensation when paid |

| Complexity | Requires careful structuring of allocations and terms | Requires valuation and adjustments to ownership percentages | Simpler structure, but depends on clear agreement terms |

| Typical use | Rewarding future contributions without giving up current value | Bringing someone in as a true equity owner | Incentivizing performance without changing ownership |

No single option works best in every situation. The right approach depends on how you balance ownership, tax consequences, and the level of complexity you are willing to manage.

Key Tax and Structuring Considerations

The structure you choose does more than define how someone is compensated. It also determines when taxes apply, how value is measured, and whether the arrangement creates issues later. These consequences are not always obvious at the outset, which is why structure matters.

- Tax consequences depend on how the grant is structured

Different forms of equity compensation are taxed differently. Some may avoid a taxable event at the time of the grant, while others create immediate taxable income. - Fair market value plays a central role

If you grant capital interests or any ownership tied to current value, the fair market value of the business becomes critical. An inaccurate valuation can lead to unintended tax consequences. - The 83(b) election can affect timing

In certain cases, a service provider may choose to pay taxes at the time of the equity grant rather than when it vests. This can reduce future tax exposure, though it carries risk if the value does not increase. - Improper structuring can create unexpected obligations

If the arrangement is not properly structured, it may result in ordinary income treatment, self-employment taxes, or other outcomes that were not anticipated. - Tax implications extend beyond the recipient

These decisions also affect how the company reports income and deductions. The structure can influence the company’s tax position as well as the recipient’s.

At this stage, the goal is not to master the tax rules, but to recognize that each option carries different tax implications. Understanding that upfront helps you approach the next step with clearer expectations.

Wrapping Up

By this point, you should have a clearer view of the incentive compensation types available to LLCs taxed as partnerships. These structures generally fall into equity-based approaches and cash-based alternatives, each with different implications for ownership and tax treatment.

The right choice depends on how you want to balance control, incentives, and long-term outcomes. Taking the time to evaluate these options carefully can help you avoid complications and move forward with a structure that fits your business.

In our forthcoming article, we will disclose how partnership-taxed LLCs can effectively leverage phantom equity and diverse cash incentives to draw in and preserve the industry's leading professionals. Stay engaged as we embark on this enlightening voyage.

Are you wondering about any of the issues mentioned above? Please email us at info@wilkinsonlawllc.com or call (732) 410-7595 for assistance.

At Wilkinson Law, we give business owners the clarity they need to fund, grow, protect, and sell their businesses. We are trustworthy business advisors keeping your business on TRACK: Trustworthy. Reliable. Available. Caring. Knowledgeable.®

FAQ

How Do I Decide Which Structure Is Appropriate for My Business?

The choice usually depends on what you are trying to achieve. If your focus is future growth without giving up current value, profit interests are often considered. If you want to bring someone in as a true owner, capital interests may be more appropriate. If you prefer to keep ownership unchanged, phantom equity may be worth exploring.

Can I Switch From One Structure to Another Later?

It is possible to change or restructure an arrangement, but doing so can trigger tax consequences or create administrative complications. Adjustments often require careful planning to avoid unintended results.

Do I Need a Formal Valuation Before Granting Equity?

In many cases, yes. If you are granting capital interests or anything tied to current value, fair market value becomes important. A reasonable valuation helps support the tax treatment and reduces the risk of disputes later.

What Happens if the Person Leaves the Company?

That depends on how the arrangement is structured. Many agreements include vesting schedules, repurchase rights, or forfeiture provisions. These terms determine what the individual keeps, if anything, when they leave.

Are These Incentives Only for Employees?

No. These structures are often used for service providers, including contractors, advisors, and key partners. The tax treatment and documentation may differ depending on the relationship.

Will Granting Equity Change How My LLC Is Taxed?

It can. Bringing in new equity holders or changing ownership percentages may affect allocations of income, reporting obligations, and how profits are distributed among members.