Key Points for New Jersey and New York Business Owners

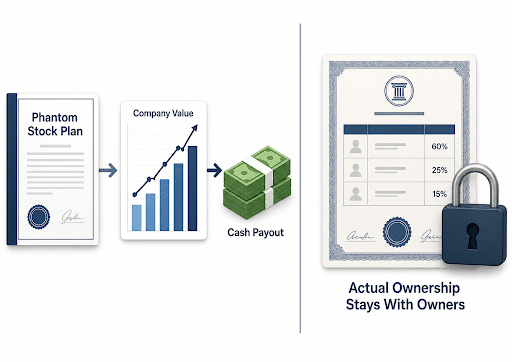

Phantom stock is not actual stock, an LLC membership, or true equity ownership.

It gives selected employees a contractual right to cash based on the company's value.

It can help retain key employees without giving them voting rights or ownership rights.

It may create tax, payroll, Section 409A, valuation, and cash-flow issues.

Business owners should review the operating agreement before adopting the plan.

The plan should define vesting, valuation, payment triggers, termination rules, and sale treatment.

If you own an LLC taxed as a corporation, you may want to retain key employees by giving them a stake in company growth without giving them actual stock ownership. A phantom stock plan can help address that tension.

Phantom equity gives the employee a contractual right to a future cash payment based on company value, vesting schedules, or performance metrics.

This article explains how phantom stock works, why tax treatment and deferred compensation rules matter, how phantom stock payouts can affect company cash flow, and what business owners should address before using phantom equity as incentive compensation.

What Phantom Stock Means for LLCs Taxed as Corporations

Phantom stock is acompensation arrangement that gives an employee a contractual right to receive cash based oncompany value, without issuing actual equity.

Under a phantom stock plan, the employee does not receive:

Actual stock or shares

LLC membership rights

Voting rights

Direct ownership rights in company assets

Instead, the employee receives phantom units, sometimes called phantom shares or shadow stock. Those units can track the company’s stock price, equity value, stock appreciation, company performance, sale value, or another formula stated in the phantom equity plan.

That separation is usually the reason business owners consider phantom equity in the first place. You may want to give key employees financial benefits tied to company growth, while avoiding actual ownership rights and the complications that can come with them.

The trade-off is that phantom stock is not cost-free. If the plan conditions are met, phantom stock payouts can create a future cash payment obligation that both the company and the owners need to plan for.

How Phantom Stock Works in Practice

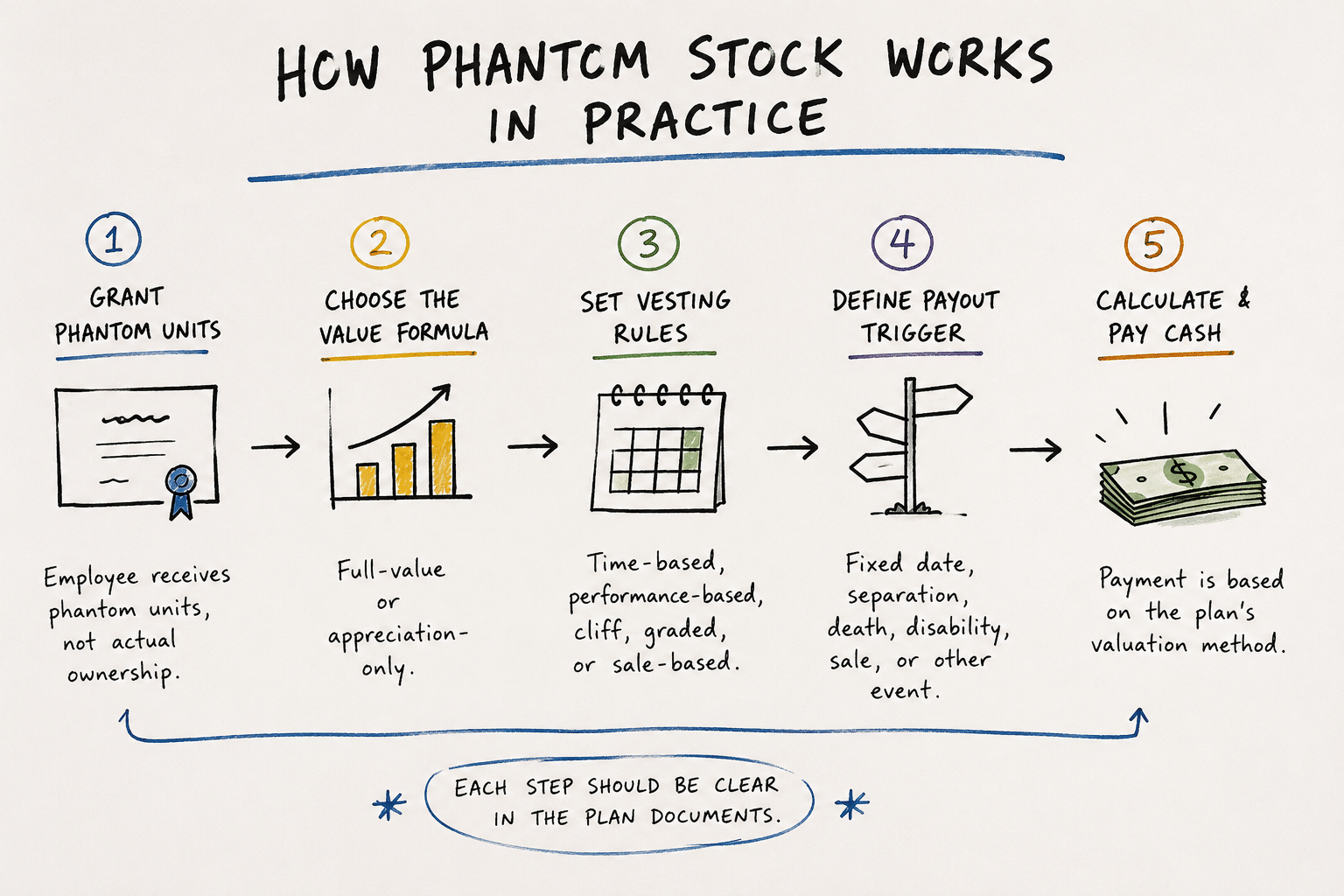

A phantom stock plan should explain what the employee receives, how the value is measured, when the right is earned, and when phantom stock payouts become payable.

The first question is what the employee is actually receiving. In a phantom stock plan, that usually starts with phantom units, which are used to measure the employee’s future cash right without issuing actual stock.

Phantom Units

The plan usually starts with phantom units. These are bookkeeping units, sometimes called phantom stock units or phantom shares, that track company value without becoming actual shares. The employee has a plan-based right, not actual company stock.

Full-Value Phantom Stock

Full-value phantom stock pays based on the full value of the phantom unit at the payment date. If one phantom unit is worth $100 when payment is triggered, the plan may pay $100 for that unit, subject to the plan terms.

That structure can be attractive when you want to give key employees meaningful financial benefits tied to company growth. It can also become expensive if the company’s stock price or equity value rises faster than expected.

Appreciation-Only Phantom Stock

Appreciation-only plans work differently. The employee receives value only above a baseline amount set in the phantom equity plan. If the baseline is $40 and the later value is $100, the payout may be based on the $60 increase.

This structure can feel closer to stock appreciation rights or traditional stock options because the employee benefits from future appreciation, not the full existing value of the business. It may be a better fit when the goal is rewarding future growth.

Vesting Schedules

Vesting schedules decide when the employee earns the phantom stock benefit. A vesting period can be designed around continued service, company performance, or a future business event, depending on what the company is trying to encourage.

Common vesting approaches include:

Time-based vesting

Performance-based vesting

Cliff vesting

Graded vesting

Sale-based vesting

This part of the plan deserves close attention. If the vesting language is unclear, both the company and the employee may later disagree about whether the phantom equity recipient has earned the right to payment.

Payout Triggers

Vesting and payment are not always the same thing. A key employee may vest in phantom units before receiving any cash payout, especially if the plan is designed to pay only after a later event.

That distinction matters for company cash flow. A vested phantom unit may represent a real future obligation, but the plan still needs to say when the company must actually make the cash payment.

Valuation Method

Private companies do not usually have a public stock price that everyone can check. For that reason, the phantom stock plan should define how company value, equity value, or the company’s stock price will be measured.

The plan may use:

An outside appraisal

A formula based on company value or equity value

Sale price or transaction value

Board, manager, or member determination

Another method stated in the phantom equity plan

Valuation is where a simple incentive idea can become a dispute. If the plan does not explain how phantom stock payments are calculated, the employee may expect one number while the company’s balance sheet supports another.

Phantom Stock vs. Stock Options, SARs, and Cash Bonuses

A phantom stock plan is only one way to structure incentive compensation. Before you use it, it helps to compare it with the tools business owners often hear about when they are trying to retain key employees.

Tool

Actual Ownership?

How the Employee Benefits

Main Business Issue

Phantom stock

No

Cash payment based on company value or appreciation

Creates a future cash obligation and may raise deferred compensation issues

Cash payout, or equity value based on appreciation

Valuation, payment timing, and Section 409A still matter

Cash bonus

No

Cash payment based on performance metrics

Simpler, but usually less tied to long-term equity value

Tax Treatment, Section 409A, Payroll, and Cash-Flow Issues

Phantom stock avoids giving the employee actual ownership, but it usually does so by creating a future compensation obligation. That is the trade-off. The company may preserve voting control and ownership percentages, but it still needs to plan for tax treatment, payment timing, payroll handling, and the cash needed to satisfy the payout.

Section 409A May Control Payment Timing

Section 409A matters because phantom stock separates vesting from payment.

This is why vesting and payment timing need to be separated in the drafting. An employee may vest after three years, but the plan may not pay until a later sale, separation from service, fixed date, or other permitted event.

If the plan leaves payment timing open-ended or lets the company freely delay or accelerate payment later, the plan may create tax problems.

The plan should define:

When the employee vests

When payment is made

What events trigger payment

Whether payment can be delayed

Whether payment can be accelerated

What happens after separation from service

What happens on a sale or change in control

The practical issue for the business owner is control. A company may want to “figure out payment later,” especially if cash flow is uncertain. But phantom stock should not be drafted as an informal promise to pay whenever management decides. If deferred compensation rules apply, payment timing needs to be built into the plan from the beginning.

The Payment May Need to Run Through Payroll

If the phantom stock recipient is an employee, the payout may need to be treated as wages. That means the company may have withholding, employment tax, and reporting obligations.

This matters because the employee may expect the full phantom stock amount to be paid directly. The company may instead need to withhold taxes and report the payment as compensation. If that expectation is not managed in the plan documents, the payout can become a dispute even when the formula itself is clear.

The plan should make clear whether stated amounts are gross amounts, how withholding will be handled, and whether the company has the right to reduce the cash payment by required tax withholding.

The Cash Obligation Can Become Expensive

If company value rises, the phantom stock payout may rise with it. That can be good for retention, but it can also create pressure if the payment becomes due before the company has cash available.

This issue often appears when:

Company value increases faster than expected

Several employees vest around the same time

Payment is triggered by termination, retirement, death, or disability

The plan requires payment before a sale or liquidity event

The payout formula uses headline sale value instead of net proceeds actually received

Why the Operating Agreement Still Matters

Even when an LLC is taxed as a corporation, itsoperating agreement may still affect whether the company can adopt a phantom stock plan and who mustapproveit before promises are made to key employees.

Before adopting a phantom equity plan, review whether the operating agreement addresses:

Who can approve a phantom stock plan

Whether manager or member consent is required

Whether equity-like compensation is permitted

Whether the plan affects sale proceeds or distributions

Whether transfer or ownership provisions are affected

This review matters because document conflicts usually surface at inconvenient moments. A key employee may leave, members may disagree over approval authority, or a buyer may ask whether phantom stock payouts were properly authorized by the company.

What Happens to Phantom Stock When the Company Is Sold?

A phantom stock plan should define what counts as a sale and how the payout is calculated before the company enters a sale transaction. Otherwise, phantom stock can become a dispute at the exact moment you are trying to close.

The plan should define whether these events count as a sale:

Triggering payment is only part of the issue. The phantom equity plan should also say whether the payout is based on the headline purchase price, net proceeds, closing cash, installment payments, or amounts actually received.

Buyers usually want to know who has a right to sale proceeds or sale-related employee compensation. If the phantom stock plan is unclear, the issue may delay due diligence or create disagreement over what the company owes.

How Wilkinson Law LLC Can Help

AtWilkinson Law LLC, we help New Jersey and New York business owners make legal decisions that affect ownership, employee compensation, governance, and future sale planning. If you are considering phantom stock, we can help you understand whether the plan fits your business before you make promises to key employees.

We can help you:

Review your operating agreement to help determine who can approve a phantom stock plan and whether member or manager consent is required.

Compare phantom stock with stock options, stock appreciation rights, cash bonuses, and other incentive compensation tools.

Structure the phantom equity plan around the business goal, such as retention, company growth, or sale-value participation.

Address what happens if the employee leaves, the company is sold, or phantom stock payouts become due before a liquidity event.

Coordinate with tax professionals on ordinary income treatment, payroll withholding, deferred compensation, and Section 409A issues.

Draft or revise plan documents so the employee understands the financial benefit without confusing phantom stock with actual ownership.

Before adopting a phantom stock plan, the legal documents should match the business promise. That is where careful planning can help you reward key employees while protecting company control, cash flow, and future transaction options.

FAQs

Can an LLC Taxed as a Corporation Offer Phantom Stock?

Yes. An LLC taxed as a corporation can use phantom stock as a contractual cash compensation arrangement, but business owners should review the plan for tax, payroll, operating agreement, valuation, and deferred compensation issues.

Does Phantom Stock Make an Employee an Owner?

No. Phantom stock usually gives an employee a contractual right to receive cash based on company value. It does not provide actual equity, voting rights, membership rights, or ownership in company assets.

Is Phantom Stock the Same as a Profits Interest?

No. A profits interest is generally associated with partnership-taxed LLCs and usually involves an actual ownership interest. Phantom stock usually creates a cash payment right without making the employee an owner.

How Is Phantom Stock Taxed?

Phantom stock payouts are generally taxed as ordinary compensation income when paid. The company may also have payroll withholding obligations. Specific tax treatment should be reviewed with a CPA or tax advisor.

Does Section 409A Apply to Phantom Stock?

Section 409A may apply because phantom stock often involves deferred compensation. The plan should define payment timing carefully and avoid informal changes that could create adverse tax consequences.